charts & data | 2023.04.12

How the pandemic impacted China Railway’s HSR network and the post-pandemic outlook

There are many misconceptions about the finances and economics of China’s high-speed rail (HSR) network. Not everyone can understand a financial statement and even fewer can go through ones that are only available in Chinese under Chinese accounting standards. Moreover, HSR is just one part of a larger rail company with a relatively complex structure. This update is part of an ongoing attempt to make the financials more clear and accessible to those who are interested in understanding China’s high-speed rail network.

China State Railway Group Company Ltd. (“China Railway”)1 owns and operates China’s passenger rail network (both conventional and HSR) and most of China’s rail freight network. Several years ago I had done a deep dive into China Railway’s financials to understand its underlying profitability and unit economics. Later, I had updated it through 2019 to support analysis on the HSR network in 2020.

This most recent effort updates financials for the pandemic period (2020 and 2022)2 and provides a glimpse of what the financials may look like in a post-pandemic environment.

Some key observations:

As expected, the pandemic really crushed passenger revenue. Ridership dropped 39% in 2020, recovered moderately in 2021 before falling another 36% in 2022 due in large part to the last salvo of strict zero-COVID policies.

Riders continued the multi-decade trend of migrating from conventional rail to high-speed. Today, over 80% of rides and over 90% of passenger revenue are derived from the HSR network.

Freight revenue saw relatively strong growth during the pandemic with an acceleration in the shift of conventional track usage from passenger to freight. This partially offset revenue decline in the passenger network.

The overall decline in top-line revenue led to a decline in profitability. China Railway’s operating margins declined from 17% in 2019 to an estimated 10% in 2022. I am forecasting it to recover to 15% in 2023 and 17% in 2024.

In 2023, robust recovery in passenger travel and continued growth in freight will drive overall revenue to surpass pre-pandemic levels for the first time. Continued recovery in passenger travel will drive overall passenger revenue to surpass pre-pandemic levels for the first time in 2024.

(1) Pandemic impact on domestic travel, passenger ridership and revenue

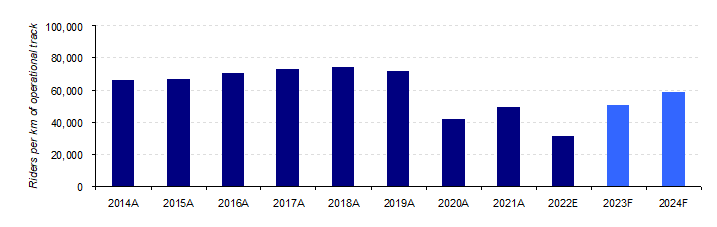

China’s passenger rail network entered 2020 on a high note. Overall ridership had grown at an annualized rate of 9% a year from 2014 to 2019. HSR ridership had grown at a scorching 21% over the same period, reaching an all-time highs in both riders (2.3 billion) and capacity utilization.

The pandemic impacted public transportation networks around the world and China was no different. The initial wave of COVID restrictions shut off New Year’s travel in 2020. While there was a rebound in domestic travel in 2021, another round of zero-COVID restrictions led to another steep decline in 2022, when HSR ridership bottomed out half of the 2019 peak.

(2) The pandemic accelerated the multi-decade trend of passengers choosing HSR over conventional rail

This translated directly into a proportional decline in passenger revenue:

By 2019, HSR already made up the majority (64%) and the vast majority (83%) of passenger revenue. This continued a trend that had started as soon as the first HSR line was opened in 2007. Conventional passenger ridership peaked in 2014 as the rise in disposable incomes had made HSR more affordable.

Notably, the pandemic accelerated this transition. By 2021, 76% of train rides were via HSR, meaning that over 90% of passenger revenue was attributable to HSR. For all intents and purposes, passenger rail travel today in China is synonymous with HSR travel.

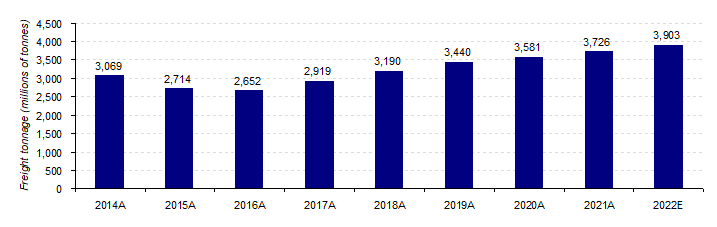

(3) Robust growth of freight during the pandemic partially offset the decline in passenger revenue

The sharp decline in passenger revenue was partially offset by healthy growth of the freight network:

Following the commodities bust of 2014-15, bulk freight tonnage declined in China as domestic coal shipments via rail declined after two decades of unfettered growth. But since bottoming out in 2016, the freight network has grown steadily with growth in tonnage continuing even through the pandemic.

The decline in conventional passenger ridership and increase in freight capacity was not just a coincidence. As HSR replaced conventional lines, existing conventional track was freed up for freight usage. Indeed, this was a key goal of the HSR build-out plan, as described here by the World Bank:

The high-speed passenger dedicated lines (PDLs) would form four horizontal and four vertical corridors linking all major cities. Except for the Hangzhou–Shenzhen corridor, all the main corridors paralleled existing conventional lines, which were either at or approaching capacity. It was difficult to purchase tickets at short notice, and long-distance trips were given priority over short-distance ones. The plan was that all long-distance passenger traffic would transfer to the new services, leaving only a limited number of local services on the existing lines and thus providing a large increment of capacity for expanded freight services.

By limiting domestic travel, the pandemic and zero-COVID policies accelerated the repurposing of conventional track to the freight network, expanding the country’s overall freight capacity.

(4) Revenue decline led to a decline in profitability during the pandemic period, but China Railway has remained profitable on an operating income basis

Contrary to popular belief, China Railway is profitable on an operating income basis. Profitability peaked in 2019 with rapid HSR growth driving strong growth in passenger revenue while freight also grew as new capacity opened up on former conventional passenger track. In 2019, China Railway achieved operating margins of appoximately 17%.

Profitability itself is a tricky concept for a state-run company running a public transportation system that generates significant positive externalities for society, such as the reduction of pollution (vs. alternative transportation methods such as driving and flying) and urban development through agglomeration.

These positive externalities are typically directly proportional to ridership which means the objective is to maximize ridership instead of say equity returns. While financial profitability could be maximized with more sophisticated pricing strategies, if it leads to lower ridership, society loses out from some of positive externalities.

Historically, both freight and passenger pricing at China Railway were set to generate enough revenue to pay for all operating costs (including depreciation) and pay a financial return to bondholders and banks. Profits to equityholders (i.e. the state) were typically de minimis. During the pandemic period, when ridership dropped sharply, China Railway could not fully cover all interest expenses to bondholders. I expect that once domestic travel returns to normal, China Railway will generate enough operating income to pay interest on its all of its bonds and loans.

(5) In 2023, overall revenue should surpass pre-pandemic levels driven by robust recovery in domestic travel and continued steady growth in freight

With the onset of the pandemic, operating margins have declined to 10%. While this is not enough to cover interest expenses (~18% of revenue), with expected recovery in domestic travel, I expect a rebound in profitability in 2023 and continued improvements in 2024.

The 2023 forecast for the rebound in passenger travel was based on a 2.7 billion passenger forecast by China Railway. This is in line with growth in ridership of 66% in the first quarter of the year to 753 million passengers. While this represents overall passenger traffic that is still below the peak in 2019 — an indication that things are not fully back to normal yet — the HSR portion of this number will be close to the 2019 figure of 2.3 billion.

The forecast for passenger ridership in 2024 (3.2 billion) still assumes that passenger activity has not topped 2019 and assumes ridership about 20% below 2019 levels when adjusted for total track. This could prove to be a very conservative assumption.

Until June 2019, known as China Railway Corporation. It is a wholly owned state-owned enterprise with the Ministry of Finance as its investor. China Railway is a holding company with multiple subsidiaries: for the passenger network, they are typically subsidiaries that operate a specific geographic region. These passenger network subsidiaries are typically owned 50% by China Railway and 50% by the local operator.

The predecessor organization to China Railway Corporation was the Ministry of Railways. In March 2013 (largely in response to the Wenzhou accident) the Ministry of Railways was re-organized into three main entities, primarily to separate regulatory responsibilities from the operational responsibilities:

Ministry of Transport — regulating safety

National Railway Administration — inspection

China Railway Corporation — operation, construction and financing of rail assets

Previous analysis relied on annual reports prepared both in Chinese and English at the holding company level - that do not appear to be distributed anymore. This analysis was prepared using Chinese-language only consolidated financials that are issued on a quarterly basis for public bondholders. There are some discrepancies that appear to be the difference between holding company and consolidated accounting.