WSJ: China’s State-Driven Growth Model is Running Out of Gas

Context and the starting point matter for these comparisons

WSJ: China’s State-Driven Growth Model is Running Out of Gas

… it doesn’t measure up to the economies China seeks to emulate. Taiwan, South Korea and Japan all opened their economies to global trade and investment, enjoyed superfast growth for several decades, then slowed as they reached middle-income status—the early 1970s for Japan, the 1980s and early 1990s for Taiwan and South Korea. In theory, China should be able to sustain rapid growth even longer because rich countries such as the U.S. have pushed the technological frontier out further, offering more room for China to catch up.

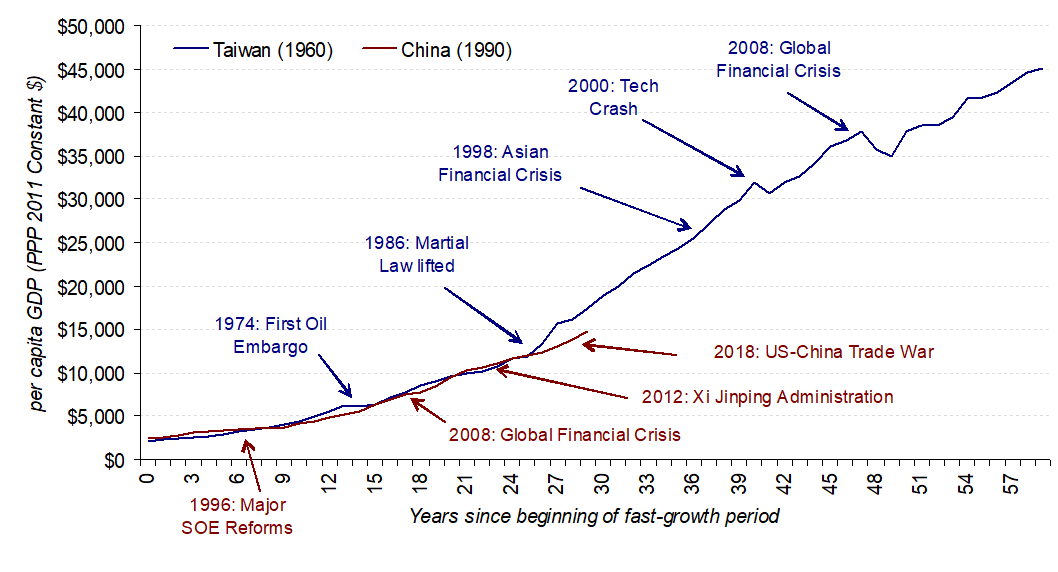

Getting the starting point right really matters if you are going to try to draw conclusions based on the per capita GDP chart in the WSJ article by Greg Ip below. Here is the chart in question:

Given the scale it’s a bit hard to tell but China’s per capita GDP at the designated starting point in 1977 is below Taiwan’s in 1960 and significantly below Japan’s in 1954. A $200 difference may not seem like a lot in absolute terms, but in relative terms it is meaningful. For example:

Growing from $250 to $14,000 in 40 years = 10.5% CAGR

Growing from $450 to $30,000 in 40 years = 11.1%.

This becomes more clear if the chart had had been presented at log-scale instead.

Pardon my photoshop skills, this is what the chart looks like if you shift the starting point for China 13 years to the left (to 1990) and update figures for 2019. The conclusions one might draw based on this might be very different from those in the article.

Thus the key question is whether 1990 is a more appropriate starting point for China in this context, noting that Taiwan in 1960 had gone through ~10 years of reform, beginning with major land reforms in the early 50s.

Meanwhile, China's initial agricultural reforms — somewhat comparable to Taiwan's land reforms — were launched in the early 80s. Giving it a decade to sink in puts you right around 1990. If you look at other metrics, you would also come to the same conclusion.

In other words, China in 1990 was arguably at a more “similar stage of development” to Taiwan in 1960 and there is a good case to be made for 1990 to be the more appropriate starting point.

Yes, China needs to follow a different path from Taiwan, South Korea and Japan. As I wrote here, because of its scale, China cannot “export its way to wealth” like its predecessors did.

Indeed over the past dozen years, China has started to go down its own path. It has reduced reliance on exports since the GFC shock. More recently it has started to (slowly) shift away from debt-fueled infrastructure spending.

As I write here, China’s path to becoming a fully developed country and avoiding the “middle income trap” will depend on its ability to tap into its large domestic consumer economy to drive innovation.

From this perspective, while the respective approaches and underlying philosophies are vastly different, the closest comparable (perhaps somewhat ironically) may actually be the US.

China is still in 3rd or 4th inning of adjusting its economy, and it is a bit too premature to come to a definitive conclusion that its approach is a failure or that it is destined to be stuck in the “middle income trap”.

Addendum

Here is the chart built using the same data (i.e. per capita PPP GDP in constant 2011 dollars) but using 1960 and 1990 as the starting points for Taiwan and China, respectively.

As discussed in the Twitter thread, using a log-scale would be a better way of comparing the two time series:

Finally, here is the comparison if you started Taiwan in 1950 and China in 1979. As discussed in the Twitter thread above, 1950 and 1979 are much more comparable starting points:

Taiwan passed its landmark land reform program in 1949, which led to major improvements in agricultural productivity and helped kickstart the “Taiwan Miracle”.

China began implementing its own version of land reform in 1979, instituting the “household responsibility system” and undoing the disastrous collectivization policies of the prior era. Similarly, this led to major improvements in agricultural productivity and laid the foundation for China to begin its modern industrialization effort.

As I said, choosing the right starting point really matters for this type of analysis.

Finally, on top of the issue with choosing the right starting point for comparison, a few other related points that are worth pointing out in response to the premise in the article that China is “slowing sooner than the others”, the implications on its future growth trajectory, and its applicability (or attraction) as an economic model for developing countries:

Degree of difficulty — Economic reforms are much more difficult to implement at the scale of China (1 billion plus people) than Taiwan or South Korea (20–50 million). For one, it takes more time to implement reform. While Taiwan could implement its nationwide land reform program in one fell swoop, the approach on the mainland was to first implement an experimental program at the provincial level and analyze the results before rolling out the program across the country (three years later). I discuss this “cadence of reform” in more detail in another post. The major implication here is that the baseline expectation for China’s growth trajectory should be lower than the others. So growth rates slowing earlier than the prior examples may be less a function of its strategy “running out of gas” and more a function of taking longer given the higher degree of difficulty. Another way one might adjust for this “degree of difficulty” difference is to compare the growth trajectory of Taiwan to a province (e.g. Fujian) instead of the entire country.

Japan as a comparable — Japan in 1954 is not a great comparable for China. Like Western Europe, Japan had already industrialized in the first half of the 20th century so even though the island country was devastated during World War II, the institutional knowledge on how to rebuild the country was still largely there. Supplemented by U.S. support and financial aid, this made the economic challenge very different in nature by those faced by Taiwan and South Korea (and China), whose economies were predominantly based on subsistence agriculture. Post-war reconstruction is very different from scaling the first rungs of economic development for the first time. If anything, the better comparable for modern China would be Meiji-era Japan in the latter half of the 19th century (and early 20th) when it was undergoing its original industrialization process.

There are no more roadmaps — This is a point that I discussed above, but it is worth emphasizing again. Starting around a dozen years ago, China began to go down its own development path. It could not “export its way to wealth” like South Korea, Taiwan and Japan, a point that was driven home in the aftermath of the Global Financial Crisis. The strategy it took — first to pour state resources into infrastructure investment and later shifting the growth focus to domestic consumption — is largely unprecedented, especially at the scale we are talking about. So it is foolish to state definitively that China will be successful going down this path … and it is equally foolish to proclaim that it is destined to fail.

As Yogi Berra said, “it’s tough to make predictions, especially about the future”. The best we can do is look at the data, try to use the right models and mental frameworks and interpret things with our best judgment.

This was originally published on Quora and on Twitter in July 2019.