Will India be able to avoid the "Middle Income Trap"?

Going from a poor to middle income country is not easy; getting rich is even harder

Going from a poor country to a middle income country is not easy. The majority of countries that were poor fifty years ago are still poor today. And once a poor country makes it to “middle income” levels, breaking out of the “middle income trap” has proven to be even harder.

In the post-WW2 era, you can count on two hands the number of economies that have been able to do this. These include:

Small island countries that rely on tourism

Trading entrepôts (e.g. Hong Kong and Singapore) that leveraged their advantageous geographic position

Resource-rich countries (e.g. Qatar) whose economic development paths are virtually impossible to emulate for larger, more diversified economies like India.

Besides these, you are really just left with two examples: South Korea and Taiwan and potentially (but not yet) China.

Today, India is still a low-income country that needs to take the first step of getting to “middle income” levels before worrying about breaking out of the “middle income trap”. I am hopeful that India is able to accomplish both one day. The stakes are high with India representing one-sixth of humanity. Lifting one billion Indians into the global middle class can only be a net positive for the world.

But the realist in me knows that there will be significant challenges ahead. Specifically, I believe developing its manufacturing sector is both absolutely necessary and key to India elevating itself into the “middle income” tier over the next two decades and then hopefully one day breaking out as well.

Looking to the past to see the future ...

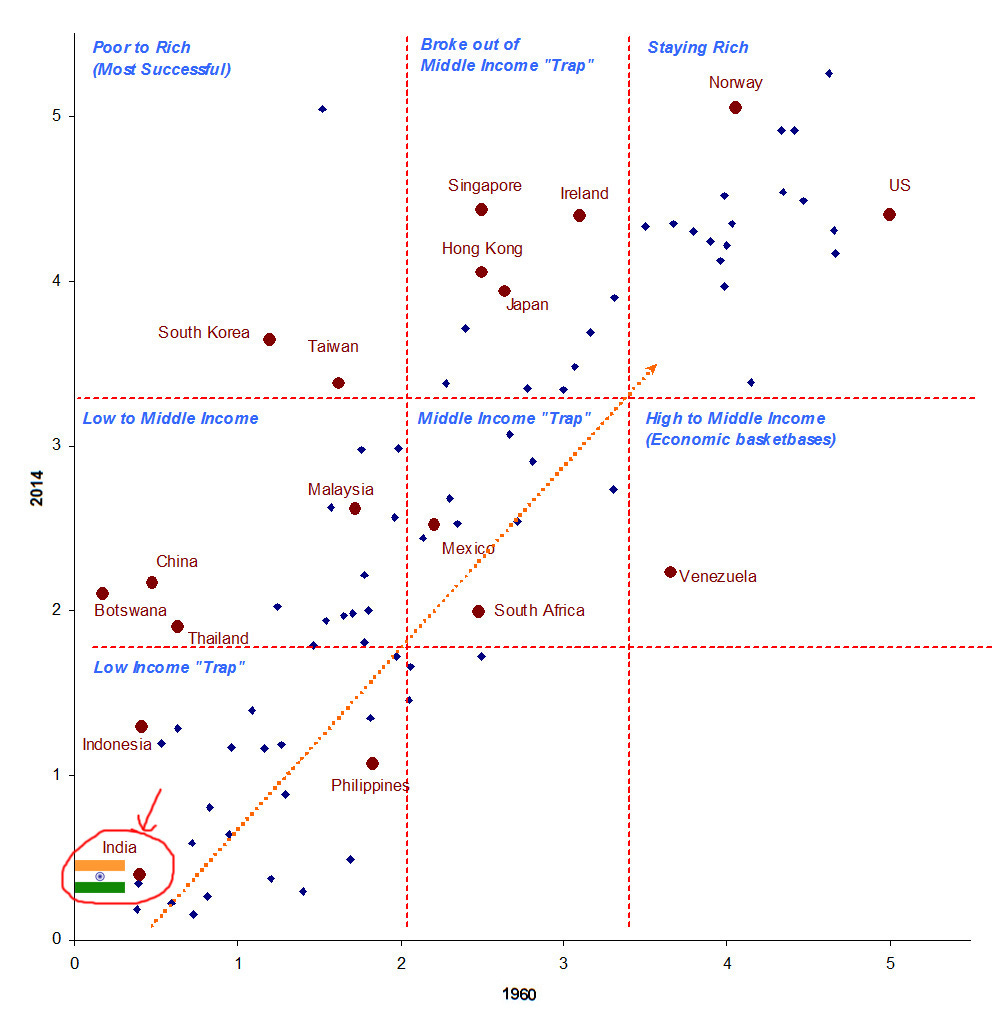

To put things in perspective, I re-constructed the Economist chart and updated the data for 2014 (see Note 1 below for my data sources and methodology). First, I looked at the data from 1960 which is similar to the original Economist chart:

As you can see, South Korea and Taiwan stand out in the upper-left quadrant as countries that were able to go from poor to rich in a little over 50 years (the other blue dot in that quadrant is Qatar, now one of the wealthiest countries in the world on the back of its massive natural gas reserves).

I’ve also highlighted some other relevant countries. In the “Low to Middle Income” quadrant, we see China and Malaysia as well as Africa’s biggest success story, Botswana. In the “Broke out of the Middle Income Trap” quadrant, we see trading entrepôts Singapore and Hong Kong as well as Japan and Ireland.

Then moving to the lower-left quadrant we have “Low Income Trap” countries. This is where India sits, although I would note the importance of staying to the left of the diagonal orange line [2]. Poor and middle income countries that sit to the right of that line are not doing well – you can see his with the troubled economies of the Philippines, South Africa and (especially) Venezuela. The good news is that India is sitting well to the left of this orange line, which means that there has been some progress.

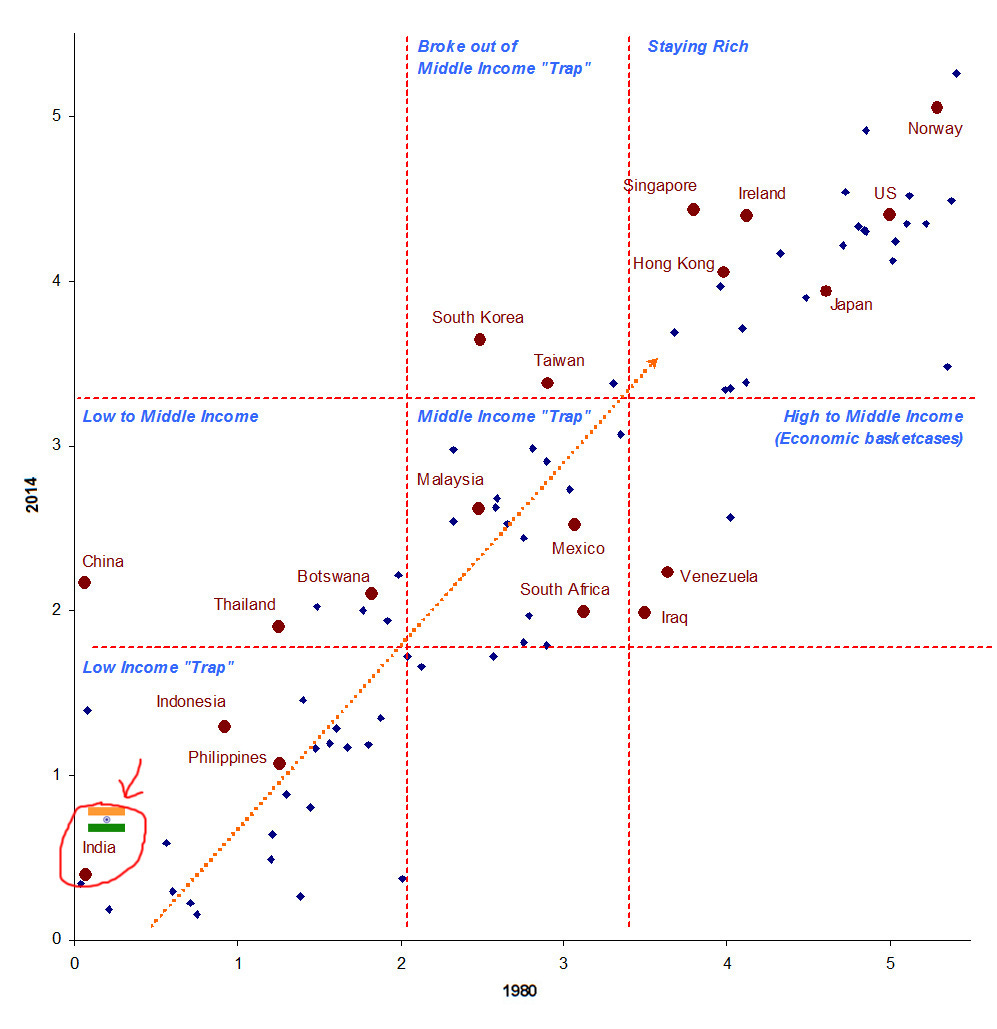

Then I re-calculated this chart to compare things in 1980 to 2014 to see how the chart changed if we looked at a shorter time horizon – one that is also more relevant for China and India which started their economic reforms a bit later than everyone else:

Once again, you can see how South Korea and Taiwan are the only ones to have broken out of the “Middle Income Trap” [3]. In the “Economic basketcases” quadrant, you will note how Iraq has joined Venezuela following a disastrous three decades during the Saddam Hussein era.

Turning our eyes to India, we can see that it is still stuck in the “Low Income Trap” quadrant. This is not to say that it has not made significant strides since 1980 or 1991 but the data is what it is. In 1991, at the beginning of India’s reforms, its per capita GDP was 1.3% of the United States. In 2014, it had risen to 2.9%. This represents progress but there is still a long way to go.

Harnessing entrepreneurial energy the right way ...

I have thought and written a lot about this topic.

I examined why South Korea and Taiwan were so unique in their ability to raise themselves up from being “dirt poor” to “high income” in less than three generations.

I have also thought about China and the challenges it faces as it tries to break out of the “middle income trap” (Will China get stuck in the “Middle Income Trap”?).

And I spent a lot of time thinking and writing about why certain Southeast Asian countries were able to go from “dirt poor” to “middle income” but appear to have since gotten stuck in that dreaded “Middle Income Trap” (Why China is wealthier than Thailand, Indonesia and the Philippines).

My overall conclusion is that it has less to do with political orientation, specific economic approaches, how well-endowed you are with natural resources, or how homogeneous your population is. And while specific things like land reform and industrialization policies seem to have mattered a lot, a more complete “grand unifying principle” was this:

Every country has enough entrepreneurial energy. The difference between success (getting rich) and failure (staying poor) lies in their ability to harness this energy in a manner that was not only profitable for the entrepreneur but beneficial to society at large.

India cannot get there on Services alone ...

The IT/BPO services exports industry is the one sector in India that is a great example of this “grand unifying principle”. Entrepreneurs who entered this sector have made fabulous amounts of money but even more importantly, their companies have generated very valuable and high-paying jobs for millions of workers, pushed this workforce to improve its skills and talents and created positive spillover benefits for the rest of the economy. Many Indians have been direct beneficiaries of this over the past two decades.

But one sector alone will not be able to make India rich, or get it to “middle income” levels even. The three million Indians that work directly in the IT/BPO sector simply cannot pull a nation of one and a quarter billion into “middle income” status on their own. There needs to be more.

In his 1998 book, Debraj Ray articulates well why India’s services-centric economy may be less the result of a vibrant services sector than an under-performing manufacturing sector:

... the enormous services sector in developing countries is symptomatic of the development of the unorganized or informal sector... This sector is the home of last resort – the shelter for the millions of migrants who have made their way to the cities from the rural sector. People who shine shoes, petty retailers, and middlemen: they all get lumped under the broad rubric of services because there is no other appropriate category.

Outside of the IT/BPO export sector, the rest of the Indian services sector consists largely of low-paying informal jobs that simply cannot support a middle class lifestyle. While the IT/BPO sector’s three million workers punch way above their weight, these industries still contributes less than 10% of India’s GDP. To lift the other billion or so Indians who are not directly or indirectly tied to the IT/BPO sector into the middle class, you need to figure out other areas where they can find ways to link them to the global economy.

There are productivity limits to services jobs. Wages for Indian IT/BPO workers shot up in during the 2000s and very quickly converged with developed country standards. But the laws of economics dictate that future wage gains will be limited to developed country growth standards, where 2% real growth per year is the “new normal” if not upper bound. In addition, we are seeing how BPOs in countries like the Philippines are today quite competitive with India.

Industrial and manufacturing businesses are not subject to the same productivity constraints that typical service sector jobs are. This is because over time you can gradually introduce more capital and technology to improve productivity year by year in small chunks over a long, long period of time. These small year-over-year productivity improvements ultimately lead to remarkable leaps in productivity over long stretches of time. In his most recent annual letter, Warren Buffett talks about the remarkable productivity improvements he’s seen in his beloved rail sector:

In 1947, shortly after the end of World War II, the American workforce totaled 44 million. About 1.35 million workers were employed in the railroad industry. The revenue ton-miles of freight moved by Class I railroads that year totaled 655 billion.

By 2014, Class I railroads carried 1.85 trillion ton-miles, an increase of 182%, while employing only 187,000 workers, a reduction of 86% since 1947. (Some of this change involved passenger-related employees, but most of the workforce reduction came on the freight side.) As a result of this staggering improvement in productivity, the inflation-adjusted price for moving a ton-mile of freight has fallen by 55% since 1947, a drop saving shippers about $90 billion annually in current dollars.

Another startling statistic: If it took as many people now to move freight as it did in 1947, we would need well over three million railroad workers to handle present volumes. (Of course, that level of employment would raise freight charges by a lot; consequently, nothing close to today’s volume would actually move.)

Our own BNSF was formed in 1995 by a merger between Burlington Northern and Santa Fe. In 1996, the merged company’s first full year of operation, 411 million ton-miles of freight were transported by 45,000 employees. Last year the comparable figures were 702 million ton-miles (plus 71%) and 47,000 employees (plus only 4%). That dramatic gain in productivity benefits both owners and shippers. Safety at BNSF has improved as well.

In contrast, if you look at output and productivity of labor-intensive service jobs like shoe-shine boys, domestic workers or retail shop workers, there is very little improvement in productivity from people doing the same things a hundred years ago.

This is why in nearly all wealthy, developed economies, huge services sectors are underpinned and enabled by a strong industrial and manufacturing base, and not the other way around.

So for India, the only way to lift itself to “middle income” status and beyond has to be manufacturing. Industrial businesses are the only way to create the hundreds of millions of relatively productive jobs that India needs to absorb the approximately 15-20 million young people entering the workforce every year.

What makes this endeavor even more critical is the risk of angry youth. If you cannot provide decent wage-paying jobs for hundreds of millions of young people, India’s demographic dividend could become a curse. Watching how things unfolded during the “Arab Spring” a few years ago, we should all have a sense of what happens when you have lots of idle, under-employed young people, especially if they tend to skew male.

Manufacturing is the key to India getting to “middle income” levels and it will also continue to play a role if India has any shot of breaking out of the dreaded “Middle Income Trap” once it gets there. It’s not going to be easy but I do believe the challenge is once again per my “grand unifying theory” of development, figuring out how to harness latent Indian entrepreneurial energy to make “Make in India” a massive success.

I discuss the specific challenges and potential solutions here in an in-depth compare and contrast between the industrial economies of China and India: Why are manufacturing costs higher in India, compared to China?

Notes

[1] Data points are based on GDP per capita (nominal) in U.S. Dollar terms (source: World Bank). I calculated each country’s per capita GDP relative to the per capita GDP of the United States and converted it to a log scale. This was similar but not exactly the same as the Economist’s approach. The classifications for “low income”, “middle income” and “high income” levels correspond roughly with the World Bank’s classifications.

I’ll note that the boundaries of these income classifications differ from the Economist chart. I don’t agree with a chart that places China at a “middle income” bracket in 1960 – it was definitely poor then.

[2] Where you are relative to the orange line in the upper-right “Staying Rich” quadrant is less meaningful.

[3] The other blue dot in that quadrant is Portugal, which was already a “Middle Income” country in 1960 and is dangerously close to falling back to “Middle Income” levels.

This was originally published on Quora in March 2016.