Why is the US behind China in moving to mobile cashless transactions?

An example of technological leapfrogging in real-time

In the U.S. — and much of the developed world — payment transaction networks are dominated by Visa and Mastercard (along with a few smaller players such as American Express and Discover). This is a classic network-effect driven duopoly/oligopoly business because once you have established yourself with merchants (e.g. payment terminals, back-end systems) and put your cards in the wallets of consumers and business users, it is virtually impossible for a new player to compete directly.

The traditional payment transaction networks do a perfectly fine job processing payments. Even though these systems rely on code that was written decades ago, the networks can still reliably process upwards of tens of thousands of transactions per second [1]. Credit and debit cards proliferated in the 80s and 90s and eventually became the dominant form of electronic payment in the U.S. and rich countries around the world, and generally made people’s lives more convenient and efficient.

As you might imagine, it also became a very lucrative business with Visa and Mastercard clipping 1 to 2% of an ever-increasing volume of credit card transactions. They worked with banks and other credit card issuers to drive usage by consumers through points and loyalty programs. Revenue and operating profits rose steadily and after going public, both Visa and Mastercard have seen their stock prices rise to all-time highs.

While the idea was novel and clever, the technology behind a modern payments platform like Alipay or Wechat Payments is not at all revolutionary. Being able to process a QR code, debit/credit ledger balances, link to your bank account, verify identity, securely process transactions etc. is not difficult. Doing it at scale is a bit more tricky but because they are not saddled with legacy code, modern payment platforms such as Alipay are able to process transactions at an order of magnitude or two — measured in the hundreds of thousands to millions of transactions per second [2] — above traditional payment networks.

I have no doubt that incumbents like Visa and Mastercard or potential new entrants like Paypal, Apple, Amazon or heck even a random team of competent software engineers can build out a similar solution, especially if they start from scratch. So why hasn’t this happened yet?

(1) Incumbents: “If it ain't broke …”

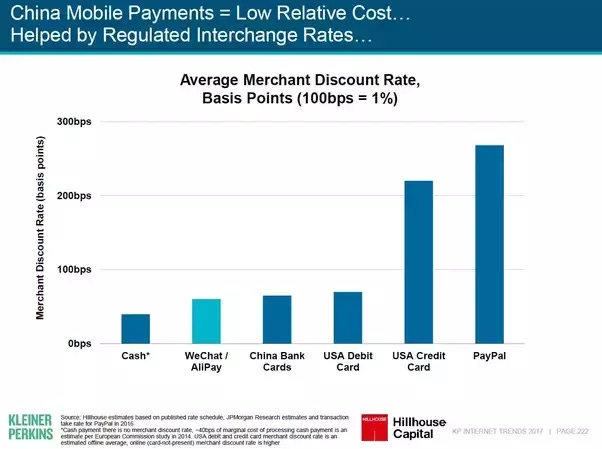

This chart illustrates the conundrum facing traditional payment network incumbents like Visa and Mastercard.

Today, they earn somewhere between 1 to 2% of each credit card transaction that is processed on their network — the chart above shows an average merchant discount of over 2%, but this fee needs to be shared with the card issuer and other players in the eco-system.

For debit card transactions processed across the same transaction network, the overall discount is significantly less than 1% — this is because debit card fees are regulated [3].

But unregulated credit card fees are much more profitable for Visa and Mastercard even if they have to share a large chunk of the fee with credit card issuers and others in the eco-system. This is the reason why points and loyalty programs have become so prevalent for credit cards but not debit cards — it is all done to push the user to opt for credit cards when paying for anything.

From a user perspective, the price and experience is more or less the same, so of course they are going to choose to pay with a credit card that earns points or “cash back” vs. a debit card that does not. The higher transaction fee is borne by the merchant which just ends up passing the cost back to consumers indirectly by raising prices. I will readily admit that despite knowing all of this I cannot remember the last time I used my debit card to pay for anything except that one time I mistakenly swiped the wrong card. Virtually all of my spending goes to the the credit card with the best rewards program — it makes the most financial sense for me and that's exactly what the credit card companies intended when they designed the system.

As evidenced in the stock charts above, this business model has been extremely lucrative for the transaction network companies and many others in the credit card eco-system.

Moving to a next-generation mobile payments platform that looks like Alipay is risky because it is not clear what the economic model looks like. In fact, it looks quite likely that the new economic model would be far less profitable — particularly in the near-term. For example, under a new system does that mean merchant fees will be regulated and lower?

Why risk cannibalizing a highly profitable revenue stream? Why mess with a formula that is already working extremely well?

Bottom line is that I wouldn't hold my breath waiting for the incumbents to lead the charge to disrupt their existing business models.

(2) New entrants: The chicken & egg problem

So it makes sense that incumbents are reluctant to move the industry to a better platform, but what about new entrants? Indeed, some of the strongest companies out there are attacking this problem — from technology giants Apple and Amazon to retailers like Walmart and Starbucks. But even they are having a really tough time making more than a small dent in the market.

First, despite impressive growth figures, transaction volume processed across these “next-generation” solutions is still very low. Recent estimates are that mobile payments make up less than 1% of total transactions [4].

Second, I put “next-generation” in quotes because these solutions are generally built on top of traditional transaction networks dominated by Visa and Mastercard. In other words, they are merely mobile front ends or digital versions of the plastic credit cards that we have always used. They are still processed through legacy credit card terminals and society still ends up indirectly paying the high credit card fees to the same small group of industry participants. Even retailer wallets like Starbucks and Walmart are usually funded by credit card payments — because users are incentivized to do so by the loyalty and rewards programs.

It is just really difficult for a new entrant to break into the market in a truly disruptive manner because it is the classic chicken-and-egg problem. Merchants need to invest real dollars and hassle into deploying new point-of-sale terminals that can accommodate new methods of payment. But it does not make economic sense to do so if <1% of consumers pay with these new methods. Meanwhile, consumers are not going to use a new payments method if most merchants don’t accept it. The existing system is “good enough” and there are also built-in incentives in place (loyalty programs) to continue the status quo.

If giants like Apple and Amazon are only able to make very small headway into the overall payments landscape (and even then, they still need to work and share fees with traditional networks), how can others that are not as well-capitalized ever hope to be successful?

Why things happened differently in China

As I described in detail in another answer (Why aren’t credit cards popular in China, the world's second largest economy?), Alipay did not face the same constraints that new entrants in the U.S. and other economies where credit card penetration and usage was already high and well-established. Once smartphones became ubiquitous in cities, Alipay rapidly expanded across the country, ultimately enabling the Chinese economy to skip the credit card stage and move straight to a superior technology that was built from the ground up for a modern digital-centric and mobile economy.

Interestingly, the proximate, near-term implications of the move are not all that revolutionary. The leap from paying with your phone vs. a credit card is much smaller than the leap from paying with cash. As mentioned above, this is one reason why U.S. consumers aren’t as vociferous in demanding a mobile solution — credit cards are “good enough” for most.

But the second and third-order effects of adopting a next-generation mobile payments solution may have much greater implications in the long run:

First, because the merchant fee is much lower for mobile payments in China than credit card payments in the U.S. this reduces the friction costs of commerce. Instead of paying 3% fees, merchants pay less than 1% and can re-invest that 2% savings back into the business or pass on the savings to the consumer. Lower friction costs are one key reason why mobile payments in China alone are set to overtake global credit card transaction volume as early as this year [notes 5 and 6].

Second, next-generation mobile payments is a true “platform technology” that can enable new business models. In another answer (What does the bike-sharing mania say about the Chinese economy?) I wrote about how mobile micro-payments was a key factor in enabling the dockless bike-sharing phenomenon.

Third, China’s next-generation mobile solution is much more likely to be the platform of choice for developing countries that — like China five years ago — are primarily cash-based economies where credit card usage is not yet prevalent. Indeed, Alibaba and Tencent are leading the charge in Southeast Asia today and investing heavily in payments companies as well as related Internet and e-commerce companies.

Fourth, besides enabling new business models, true next-generation payment platforms also generate a deluge of valuable transaction data for Alibaba and Tencent — data that is significantly more granular and attributable than data that can be collected by traditional transaction networks or credit card issuers. Alibaba and Tencent are fine with the relatively low regulated merchant fee rates because what they are really after is the holy grail of data.

When technology leapfrogging occurs, it is rarely the result of an incumbent’s inability to develop new technologies. As Clay Christensen described in his book The Innovator's Dilemma, it is almost always organizational factors that create significant obstacles to the adoption of new, disruptive technologies.

In the case of the payments industry, there is a huge profit motive by players across the credit card eco-system to maintain the status quo. These companies are public companies, run by executives and overseen by boards who have a fiduciary duty to shareholders and are typically heavily incentivized to maximize the market value of the corporation. Having sat on several public and private company boards in the past, I fully understand and appreciate why it is so hard for them to embark on a path that may violently disrupt their own business model — especially one that is very successful — and why they tend to be suspicious of new entrants. These are extraordinarily rational decisions (or non-decisions) for companies like Visa and Mastercard to make.

But China circa 2013 was not hampered by the same constraints, and new entrants like Alibaba and Tencent were able to break through and completely change the paradigm. It is still early but it appears that they have built an insurmountable lead in China — one that is unlikely to be broken by any new entrant foreign or domestic — and are starting to build significant leads in places like Southeast Asia. And this is just the beginning if you buy into the idea that mobile payments is a true platform technology.

Ironically, in this new world, Alibaba and Tencent are quickly emerging as the new dominant incumbents. And in the future, it will be very interesting to see whether or not they act any differently in the face of potential future disruption.

Notes

[1] Source: Visa — 65,000 Transaction messages per second — peak capacity as of August 2016

[2] Source: Alibaba — “Alipay processed 256,000 payment transactions per second at peak within the first hour” Theoretical peak transaction volume should be significantly higher than this — really just a matter of adding more computing resources on Alibaba Cloud.

[3] Source: Durbin Amendment

[4] Source: CNET — “Today, mobile payments still make up less than 1 percent of overall in-store US transaction volume,” says Jordan McKee, principal payments analyst at 451 Research. “Our research also shows that likelihood of using digital wallets has plateaued since the launch of Apple Pay.”

[5] Source: Mary Meeker 2017 Internet Trends Report — China mobile payments volume was >$5 trillion in 2016 and still growing by over 60% a year. 2017 transaction volume is likely to be north of $8 trillion and grow to >$12 trillion in 2018.

[6] Source: The Nilson Report — “Global card purchase volume grew 5.8 percent to $20.606 trillion in 2016, according The Nilson Report.” — This $20 trillion figure includes a significant contribution from China UnionPay and debit card payments.

This was originally published on Quora in December 2017.