Why is it hard for other auto insurance companies to copy GEICO's low-cost model?

GEICO has evolved over the years

When GEICO first got started, it was tiny and none of the traditional insurance companies paid much attention to its relatively unique low-cost approach. This was during the post-WW2 boom era and the others were too busy trying to grab their share of the emerging American middle class, who were just beginning their lifelong love affair with the automobile.

By the time GEICO had become large enough to garner some notice, it’d had the benefit of several decades of experience refining its unique business model. While the company did stumble along the way in the mid-70s , it was able to recover and ultimately get better as a company.

When other automobile insurance companies started seriously exploring the power of the direct marketing model, GEICO had already achieved scale. This scale became a source of durable competitive advantage in and of itself: Today, GEICO’s position as the second-largest auto insurer allows it to outspend the competition in building its brand, which ultimately adds to its “economic moat”.

Moreover, since it became a wholly owned subsidiary of Berkshire Hathaway in the mid-1990s, GEICO has added a few new unique advantages over the competition.

(1) GEICO, the Low-Cost Provider

As the question implies, most people already know of GEICO as a low-cost provider that relies on direct marketing instead of employing the more traditional and costly agent-based model.

But how big was this advantage exactly? While I have not come across the company’s detailed financials from its early years, a good guess is that this cost advantage was and continues to be in the 15% range. This is based on analyzing how much agent networks cost [1] traditional insurance companies, or more simply by referring to GEICO’s well-known jingle:

What is less well-known is that part of GEICO’s strategic advantage during its early years came from its utilization of a very targeted marketing strategy. You see, GEICO actually originally stood for the “Government Employees Insurance Company”:

Through direct mail campaigns, the Government Employees Insurance Company specifically targeted federal employees, military veterans and university professors ... the types of safe and boring customers that one would expect to avoid excessive risks while driving. This allowed early GEICO to expand rapidly without taking on risky customers that might drive up underwriting losses. After writing 3,700 policies in its first year, the company grew at a rapid pace, reaching annual insurance premiums of $150 million by 1965:

Other insurance companies did not follow GEICO’s direct business model back then because doing so would have involved completely up-ending their existing business models and letting go of the majority of their staff. There are very few companies in history have ever mustered the resolve to do something so drastic. Besides, in the grand scheme of things, GEICO was also quite tiny and in the post-WW2 growth boom, there were plenty of new American households to pursue.

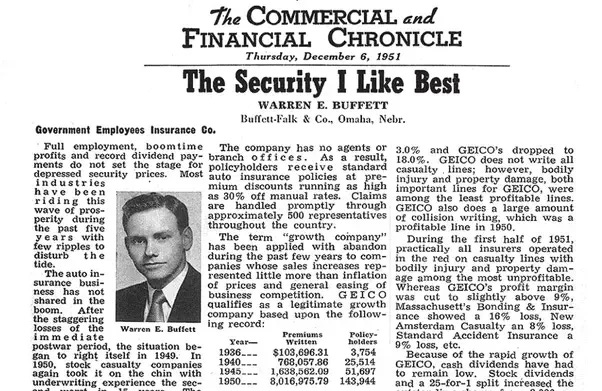

GEICO as the low-cost provider was the insurance company that Warren Buffett came across while working as a broker in the early 1950s, calling it out as the “Security [he liked] Best”:

(2) GEICO, the Brand

In the early 1970s, GEICO’s founders passed away and ushered in a period of where the company struggled. It had grown to the point where it was no longer merely targeting federal employees and the company made some missteps as it tried to aggressively expand. This aggressive expansion led to some careless underwriting which ultimately led to serious losses that almost bankrupted the company.

While GEICO’s low-cost business model still provided it with a significant cost advantage over its competitors, it had forgotten what is perhaps the most important rule in the insurance business which is to avoid “growth at all costs”.

It was at this point that Warren Buffett swooped in a second time, purchasing 1 million shares and helping right the ship. The company returned to lower but more prudent growth rates and the company was able to get back on its feet.

In 1993, Tom Nicely became CEO of GEICO and soon began to evolve its business model. Now the strategic focus became about how to build a durable consumer brand. This was virtually unheard of in the insurance industry, which was still largely reliant on the relationship-based high-touch selling model and large agent networks.

This is when American consumers started seeing quirky ads on TV such as these:

It is also when we started learning about characters like:

The Caveman (who subsequently got his own spinoff TV series):

And of course, the Gecko:

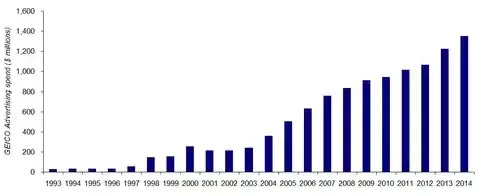

Meanwhile, Al Gore was busy inventing the Internet. And what the Internet did for GEICO was really kick its direct marketing model into high gear by providing new channels to spend advertising dollars. Warren Buffett, whose Berkshire Hathaway conglomerate now owned approximately 46% of GEICO, noticed this and bought out the rest of the company in 1996. In his 2005 Letter, Mr. Buffett reflected back on the importance of advertising and brand-building at GEICO:

While our brand strength is not quantifiable, I believe it also grew significantly. When Berkshire acquired control of GEICO in 1996, its annual advertising expenditures were $31 million. Last year we were up to $502 million. And I can’t wait to spend more.

Our advertising works because we have a great story to tell: More people can save money by insuring with us than is the case with any other national carrier offering policies to all comers. (Some specialized auto insurers do particularly well for applicants fitting into their niches; also, because our national competitors use rating systems that differ from ours, they will sometimes beat our price.) Last year, we achieved by far the highest conversion rate – the percentage of internet and phone quotes turned into sales – in our history. This is powerful evidence that our prices are more attractive relative to the competition than ever before. Test us by going to GEICO.com or by calling 800-847-7536. Be sure to indicate you are a shareholder because that fact will often qualify you for a discount.

Now, less than a decade later, GEICO is close to spending over $2 billion per year in advertising alone:

By the early 2000s, other auto insurance companies began to really notice GEICO’s robust growth and some tried to emulate their direct marketing model. Notably Progressive Insurance has invested heavily in brand advertising with similar GEICO-esque quirkiness and their own Gecko-like character (Flo). Internet-based and online-only models like Esurance entered the fray. Esurance was ultimately acquired by a traditional agent-based insurance company (Allstate) which continues to this day to allow it to run as a separate division – further evidence of how difficult (if not impossible) it is for the traditional insurers to start over from scratch.

At this point, GEICO has gotten so large that its scale had become a source of durable competitive advantage on its own. In 1993, GEICO had 1.9% [2] of the U.S. car insurance market. By 2015, it had become the industry’s second-largest player with market share rising to 11.4% [2]. Meanwhile, it has leveraged its widely recognized brand into other lines of business, such as motorcycles and motorboats. Today, its scale allows it to far outspend its competitors in advertising which then leads to even higher market share and scale.

GEICO is one heckuva business.

(3) GEICO and the Berkshire Hathaway advantage

But wait, there’s more!

Since becoming a wholly owned subsidiary of Berkshire Hathaway, GEICO has gained a few more small unique advantages.

Some of them are small, like the fact that it gets some free word-of-mouth advertising from one of the most recognizable and admired companies in the world. Mr. Buffett always gives GEICO a shout-out in his annual letter and GEICO is heavily featured at its wildly popular annual meeting, when tens of thousands of diehard Berkshire Hathaway fans flock to Omaha.

Others are more significant, like the fact that GEICO can leverage the power of Berkshire Hathaway’s pristine credit rating. In the insurance business, an insurer’s capital base and credit rating are quite important and there is no stronger insurance company than Berkshire Hathaway.

Most importantly, GEICO gets to benefit from the sharp investment acumen of Mr. Buffett and his partners. Insurance companies have something called “float” which are the premiums that they receive from customers in advance of any potential payouts. As of December 31, 2015, GEICO had about $15 billion of this float. Most insurance companies typically invest their float in relatively safe, but low-yield fixed income portfolios that might generate 6% of yield in a good year. But GEICO, by virtue of being under the Berkshire Hathaway umbrella, can invest its float in a much more interesting mix of stocks as well as entire operating businesses, all under the oversight of world’s greatest living investor. The 9% difference between generating 15% returns and 6% on $15 billion of float is equivalent to around $1.3 billion per year in incremental profit alone. And Mr. Buffett’s done way better than a 15% IRR over his lifetime of investing.

Notes

[1] From Insure.com:

Home and car insurance agents typically receive a 10 to 15 percent commission on the first year’s premium. Commissions can range as low as 8 percent, says Bissett, while “15 [percent] would be on the very high end.”

Your insurance agent could also be making money every year you renew the policy. For auto and home insurance renewals, agents make a 2 to 15 percent commission (most are in the 2 to 5 percent range). Life insurance renewal rates are typically 1 to 2 percent, or zilch after three years.

That is just for the broker. There might be additional marketing costs, like rent for branch offices.

[2] Source: Various Berkshire Hathaway Shareholder Letters

This was originally published on Quora in April 2016.