Why aren’t credit cards popular in China?

Leapfrogged

Early on (i.e. the late 1990s up to around 2012-13), the main reason credit cards weren’t popular in China was mostly related to the slow nature of credit card adoption — especially early in the cycle — coupled with the reality that China was relatively late to the development party.

But over the last five years, the key reason why credit cards have continued to remain a niche payment method in China — and are unlikely to ever be anything more — is simply that they have been leapfrogged by a next-generation payments platform that was designed from its core with the modern digital and mobile-centric world in mind. In contrast, the core of today’s credit card payments infrastructure still dates back to technologies from three to even five decades ago.

One interesting hypothetical to ponder is what would have happened if credit card use had proliferated throughout China to scale before the rise of the smartphone. Would a next-generation payments solution have risen so quickly if there was already a “good enough” solution in place that was dominated by two or three players? Or would China’s payments landscape more resemble what you see in most developed countries today?

Let’s first consider this question from the perspective of the major constituents in the credit card eco-system to understand why market adoption has generally occurred at a glacial pace, especially in the early stages.

At a high-level within the credit card system [1], you have:

Consumers

Merchants

Credit Card Issuers — someone to take on the credit risk, usually a bank e.g. Chase, Wells Fargo or Bank of China

Transaction Networks — someone to facilitate the transaction between the merchant and buyer e.g. Visa, Mastercard or China UnionPay

Now let’s re-wind back to the late 1990s, where after roughly two decades of rapid development, China’s consumer economy had just reached the point where some consumers began to start thinking of a world beyond cash. Up to this point, China was effectively a 100% cash-based economy, with payment methods looking pretty much the same as they had for the past thousand years. If you plucked someone out of 9th-century Tang-era China, placed him in a circa 2009 wet market and gave him a wad of cash, he/she could probably figure out how to buy some vegetables without really flinching.

The only merchants that might accept a credit card were places that catered to foreigners; places like five-star hotels and airports. For the other 99% of Chinese merchants, implementing a credit card system required a rather significant investment in credit card processing terminals and secure data communication lines … and as a reward for your investment, you were blessed with the “privilege” of forking over 2–3% of every transaction to an American payments company. “No thank you, we’ll stick to cash” replied pretty much every Chinese merchant.

Now from a consumer perspective, credit cards are only useful if there are places where you can actually use them. Otherwise it is just a liability made out of plastic that takes up valuable space in your wallet. Since there were so few merchants that accepted credit cards, there was also very little demand from Chinese consumers for credit cards. It was a classic chicken/egg problem.

And of course you also needed someone to actually issue the credit cards. Chinese consumers had essentially no documented credit history and all of the banks — who would normally take on the credit card issuer role — were owned/controlled by the State and had zero incentive to push credit cards to consumers [2]; this remained largely true even after China established China UnionPay in 2002 to provide a local alternative to the global and largely U.S.-dominated transaction networks. Adoption of credit cards was painfully slow, reaching less than 10% of the population after more than a decade [3].

Of course, slow adoption of credit cards was not unique to China. Indeed if you examine the development of credit card networks in the United States and Europe, you’ll find that these markets also took decades to fully develop [4].

Fast forward to four years ago. Even as recently as 2013, China was still largely a cash-based society. It was rare to find a credit card payments terminal outside of places that were frequented by tourists and foreigners. But a few things happened in quick succession that essentially jump-started the stratospheric rise of a next-generation payments eco-system in China:

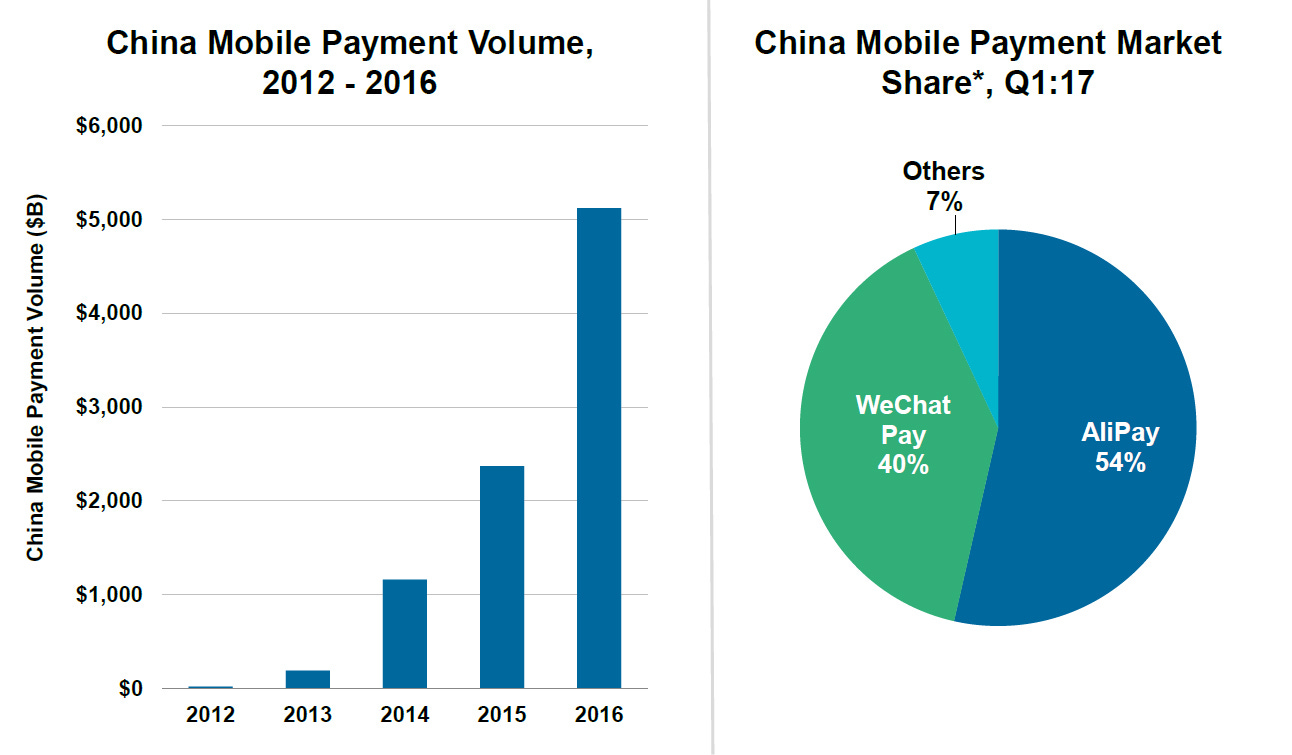

(1) Alibaba develops a next-generation payments platform for e-commerce in 2004

Alipay is a third-party payments platform that was launched in 2004 by Alibaba to facilitate e-commerce transactions on Taobao. In the early years, it was very similar to Paypal and like Paypal took a very small percentage of the overall transaction market, as it was largely restricted to the small (but fast-growing) e-commerce market. It remained relatively niche until …

(2) Smartphone adoption goes from “0 to 60” in less than four years (2010–2014)

This was the key enabling factor for a next-generation payments platform to take hold as it eliminated in one fell swoop one of the major friction areas for credit card adoption — convincing merchants to invest in expensive credit card processing technology. The processing power in a smartphone blows away the processing power in your typical credit card processing terminal. This should be no surprise, as core credit card processing technology is still based on ‘80s era infrastructure. The technology behind Alipay’s QR-code based payments system was superior to back-end credit card processing technology in the same way Apple’s iOS was superior to Symbian and Blackberry, whose core kernels had been developed before the era of data-centric wireless networks.

The ubiquity of the smartphone obviated the need to invest in expensive, clunky proprietary credit card payment terminals. Instead, now it was possible for every merchant large and small to use their smartphone as a slick payments terminal — they did not even need to install an extra device/dongle (e.g. Square) to accept payments. And consumers did not need to wait for a plastic credit card to show up in the mail and be “verified” — they already had a more sophisticated and more secure platform sitting in their pocket or purse. It did not take long for Alipay to re-focus its platform on the mobile user … and saw usage skyrocket.

Ironically, this led to an explosion in the installation of payments terminals and digital point-of-sale (POS) systems throughout the country, except that these are focused on reading the QR code-based system used by AliPay and WeChat Payments instead of credit cards (though many do as well). For merchants, most of whom did not have a credit card terminal before, this was a huge step-improvement for them and not jus for taking payments but also for general accounting, controlling shrinkage etc.

(3) Enter Social (2014): WeChat enters the fray with digital hongbao (red envelopes)

In early 2014, for Chinese New Year, China’s largest social platform WeChat launched a new feature whereby users could send each other money in the form of digital red envelopes (hongbao) by linking its (then) relatively niche WeChat Payments platform with its social/messaging plaform — which was already the most widely used app on nearly every single Chinese person’s smartphone at that point. It was an overnight sensation; within a single month, wallet adoption increased from 30 million to 100 million and today WeChat Payments supports over 600 million active users.

China’s mobile-centric digital payments infrastructure has leapfrogged the relatively archaic credit card payments infrastructure that reigns in most of the developed world. And it happened in pretty much a blink of an eye — I wrote about an eye-opening experience I had feeling like a digital luddite after a two-year hiatus where I had not visited China.

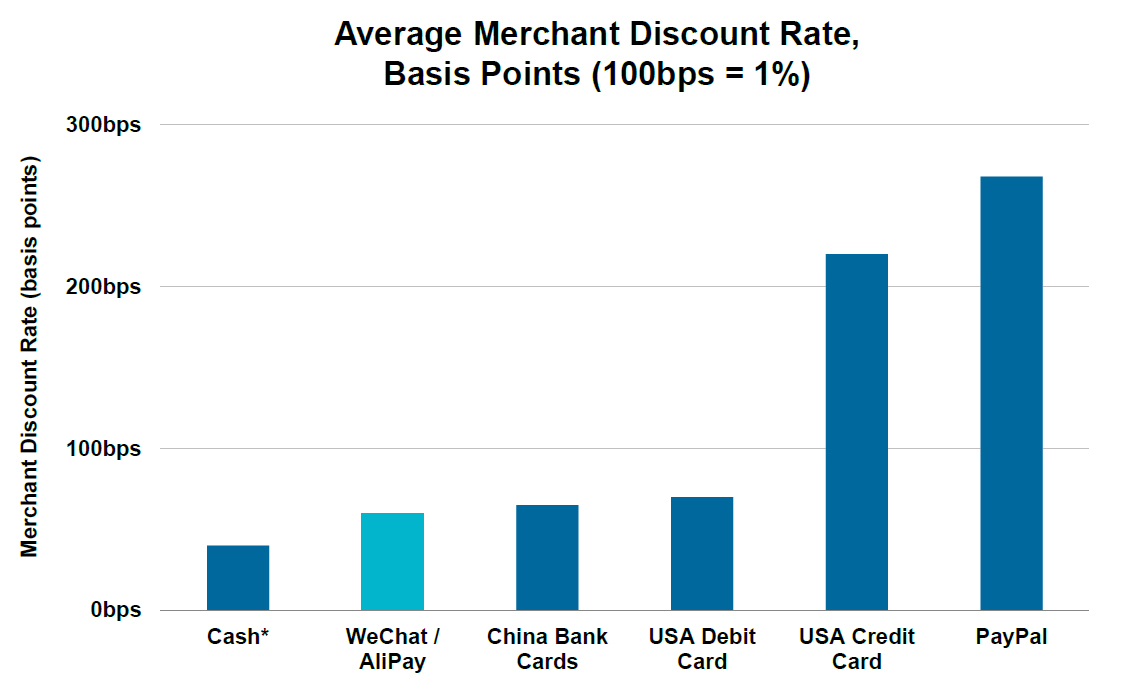

In addition, China’s next-generation mobile-centric digital payments infrastructure has accelerated the rise of offline-to-online (O2O) services adoption in China by making the payment process relatively inexpensive and friction-less. For example, the tremendous rise in bike-sharing in China is in part enabled by the ability to conduct payment transactions of as little as 1 RMB (15 cents). Current credit card economics — which are unlikely to change in my view given the duo/oligopolistic nature of the global transaction networks today — make it very difficult for transactions below a certain value to be conducted, largely because of the lower effective percentage take by the intermediary:

With its superior technology and — even more significantly — AliPay and WeChat Payments having firmly established themselves as the de facto payments method in China, at this point traditional credit card infrastructure really has no chance of ever breaking into China in a big way. There’s just no point for consumers to switch back to a platform whose underlying technology was not built for the modern mobile and digital-centric world. The real only question is how quickly the credit card companies adopt a next-generation system that looks a lot more like Alipay/WeChat Pay — and as I argue in another example, it could take a while.

Notes

[1] It is a bit more complicated than this. For example you often have a separate firm that just handles the physical payment processing piece (including the installation and maintenance of the payments terminal and related data lines) but for the purposes of this answer, we do not need to delve into that.

[2] If anything they had less than zero / negative incentive given overriding economic policy throughout this period was to focus on suppressing domestic consumption and funnel resources into investment-centric development. The correlation between today's greater emphasis on consumption-led development (beginning around 2012–13) and the rise of Alipay is very likely more than just a mere coincidence.

[3] After the establishment of UnionPay, debit card adoption was not slow, though. But that was because debit cards were merely replacements for the painfully less efficient physical bank books that only older Quorans might remember. Debit cards in China are used to conduct banking transactions (e.g. withdrawing cash from an ATM), not for merchant transactions.

[4] Credit card transaction networks follow classic network effect rules in that the overall value of the network increases exponentially as more consumers and merchants join the network. On the flipside, adoption of a network can be painfully slow in the early years because the value it creates is so low. In the United States, the first instances of charge cards (i.e. the predecessor to the credit card) appeared as early as 1921 when Western Union began issuing them to its most frequent customers. It wasn’t until 1958 when Bank of America launched the first modernly recognizable credit card and this was after multiple failed attempts across the country:

Until 1958, no one had been able to successfully establish a revolving credit financial system in which a card issued by a third-party bank was being generally accepted by a large number of merchants, as opposed to merchant-issued revolving cards accepted by only a few merchants. There had been a dozen attempts by small American banks, but none of them were able to last very long.

In September 1958, Bank of America launched the BankAmericard in Fresno, California, which would become the first successful recognizably modern credit card. This card succeeded where others failed by breaking the chicken-and-egg cycle in which consumers did not want to use a card that few merchants would accept and merchants did not want to accept a card that few consumers used. Bank of America chose Fresno because 45% of its residents used the bank, and by sending a card to 60,000 Fresno residents at once, the bank was able to convince merchants to accept the card. It was eventually licensed to other banks around the United States and then around the world, and in 1976, all BankAmericard licensees united themselves under the common brand Visa. In 1966, the ancestor of MasterCard was born when a group of banks established Master Charge to compete with BankAmericard; it received a significant boost when Citibank merged its own Everything Card, launched in 1967, into Master Charge in 1969.

In the early years, charge and credit cards were often considered fairly exclusive; for example, American Express got its start focusing on well-traveled businessmen and elite jet-setters. But with each merchant installing a credit card terminal, it became more attractive to consumers and with more consumers obtaining credit cards, it became more attractive to merchants. Network effects started to take over and eventually credit card usage became fairly ubiquitous by the 1980s — more than two decades after the first modern credit card came into existence.

This was originally published on Quora in June 2017.