Which company was the most valuable in history?

It wasn't the Dutch East India Company

One thing I am certain about is that it was not the Dutch East India Company. While huge in its time, it is not close to being “the richest company ever.” Based on my math and analysis below, it was worth somewhere between $1 and $8 billion in today’s dollars.

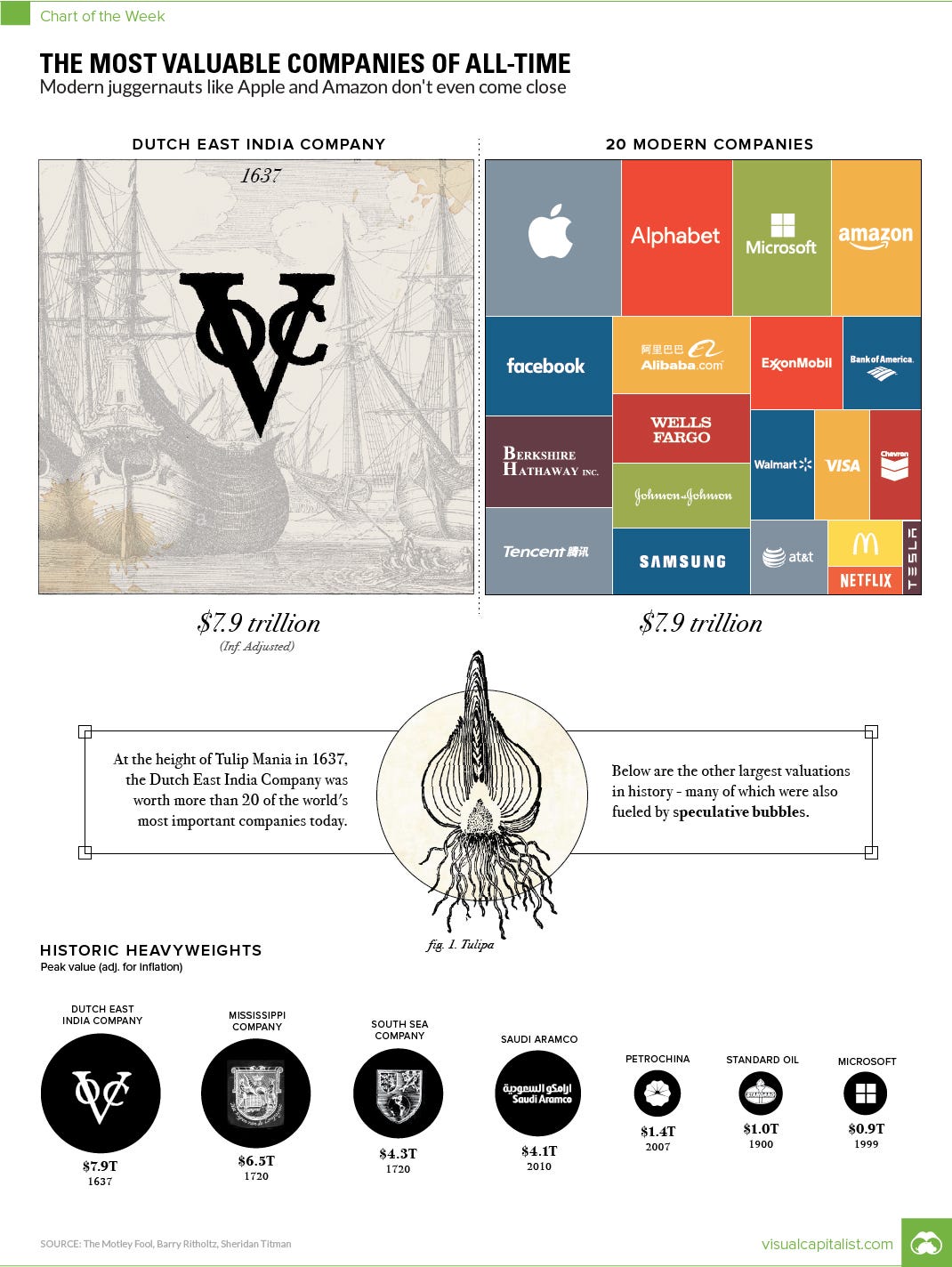

There was an infographic circulating a few years ago about how the Dutch East India Company, better known then as Verenigde Oost-Indische Compagnie (“VOC”), was worth $7.9 trillion in “inflation-adjusted” terms.

This implied that it was worth more than the largest dozen or so public companies on the market at the time, a list that includes Amazon, Apple, Alibaba, Berkshire Hathaway, Exxonmobil, Microsoft, etc.

I tried to get to the bottom of how exactly they adjusted for inflation, and traced it all the way back to a Motley Fool article from 2012 but I never did find a detailed calculation and explanation [see Note 1 below for further discussion].

But the $7.9 trillion figure seemed awfully suspect, so I did a bit of research into VOC to see if I could triangulate to a better number by examining the financial and operating metrics of the company.

Here are some relevant financial metrics for VOC:

VOC was originally capitalized with 6,440,200 Dutch guilders

VOC’s average annual profit during its “Golden Age” period (1630–1670) was 2.1 million guilders

VOC achieved a profit margin of around 18 percent (on total revenue) during the “Golden Age” period, implying annual revenue of approximately 11.7 million guilders

In 1780, VOC’s balance sheet featured total capital (net of debt) of 62 million guilders, comprised primarily of ships and inventory

VOC achieved a peak market valuation of around 78 million guilders, which was around 37x normalized earnings

78 million Dutch guilders is not worth anywhere close to $7.9 trillion of today’s dollars. This massive valuation yields an implied exchange rate of over $100,000 (2020 dollars) per Dutch guilder.

{kind=link}

It’s always a bit tricky to compare currencies from two eras that are so far apart but if you really must do it, gold is your best bet.

Indeed, “guilders” means “golden” in Dutch and we know that a Dutch guilder was equivalent to 605.61 milligrams (0.0214 oz.) of gold in the 17th century. This implies an exchange rate of $38 per Dutch guilder.

Re-stating these figures in terms of gold, VOC was worth 1.669 million oz. (~52 tons) at its peak. At the current (June 2020) gold price of $1,771 per oz., its implied market valuation is right around $3 billion.

As for corporate profitability, using the same math VOC generates around $80 million per year in annual operating profit. This is nice chunk of change but I am not even sure if it makes the Russell 1000 Index today.

At the height of its operation, VOC had 150 merchant ships and employed 50,000 people. Assuming a generous 2,000 tons per ship making one back-and-forth trip a year, the company could move around 600,000 tons.

To put this in perspective, this is the rough equivalent to the fully loaded capacity of a single ultra-large container ship, the OOCL Hong Kong, which can make the round-trip from Rotterdam to Singapore in 80 days. The OOCL Hong Kong cost around $1 billion (in 2020 dollars) to build.

Back in 17th century Holland, a typical outdoor laborer earned about 6.5 guilders per week, or 300 guilders per year. This is what the typical VOC dockhand or sailor would earn as well.

Taking the $7.9 trillion figure at face value (i.e. ~$100,000 per Dutch guilder) implies that outdoor laborers back then earned over $30 million per year in today’s dollars. Using the much lower exchange rate implied by the gold equivalent ($38 per Dutch guilder) yields a more reasonable annual income of $11,367 per year.

Looking at it from another perspective, $7.9 trillion would value VOC’s 50,000 employees at a cool $158 million each. One of the highest market value-to-employee ratios out there today is Facebook at around $13 million/employee, less than 1/10th. Given that most of VOD’s 50,000 employees were laborers relying largely on their muscles, this is likely off by at least three orders of magnitude.

A closer comparable would be Walmart which is valued at around $152,000 per employee. Applying this metric to VOC yields an implied market valuation of around $8 billion. Even this figure is optimistic, as a Walmart employee — with access to modern equipment and technology, and better educated — is significantly more productive than the average 17th-century manual laborer.

In summary, we arrive at a valuation somewhere in the $1 to $8 billion range. While it doesn’t have quite the same ring as “$7.9 trillion”, this figure looks far more realistic. And by 17th and 18th century standards, this was truly an enormous sum.

The actual “richest” company?

If measured by market capitalization, it would be Apple, which as of last Friday (June 26, 2020), had a market capitalization of $1,533 billion, just beating out Microsoft at $1,489 billion.

If we want to count non-listed companies, Saudi Aramco may be worth even more than both of them — based on its claim on 270 billion barrels of identified, easily extractable crude oil reserves.

VOC was a massively impactful company for its time, helping the Dutch Republic dominate global trade for nine “Golden” decades spanning the 16th and 17th centuries. But the idea that it would barely qualify for a small-cap index today illustrates just how much the world has progressed over the last three centuries.

Explanatory Note

[Note 1] I suspect the $7.9 trillion figure was based on an excel worksheet using an assumed inflation rate (or re-investment rate) compounded over more than three centuries. Anyone who understands compound growth over such long periods of time knows how getting this assumption even a little bit wrong could lead to wildly unrealistic outcomes.

The other explanation — as brought up in the comments section — is that the $7.9 trillion figure is derived by calculating VOC’s value vs. aggregate global wealth in the 17th century and then applying that fraction to today’s (significantly larger) number. As I discuss in the comments section, I disagree with this approach, and define wealth as being very specifically based on the production of real goods and services.

This was originally published on Quora in June 2020.

Great analysis. This would make a great basis for an economics class. Present the problem of how to value the Company in current dollars, and guide the students to the various answers if they don't come up with them. This would be good for either undergrads, MBA's, or PhD students, and it would make a fun party theme for professors.

I very much agree about "wealth as being very specifically based on the production of real goods and services": even something seemingly as directly comparable as a wheat field isn't the same, producing today 5-10 times as much as in the 17th-18th centuries. I think you're right about the bogus $8trn valuation being based on modern assets or GDP: it's the very thing that makes those ridiculous "all-time rich lists" of supposed mediaeval multi-billionaires all the more absurd.

In fact even at today's prices, the market value of all the world's economic assets didn't reach $8trn until around the 1860s, while Europe's entire 18th-century annual trade with Asia came to only 0.1% of global GDP (the VOC accounting for perhaps 0.04%) and the combined economies of the Netherlands and Indonesia to barely 2%, so the VOC's investors would have been a truly eccentric lot to plough more than the whole planet's market capitalisation into one company returning a modest annual fraction of 1% of the value of their stake.

We can come a bit closer to a vaguely serious modern valuation: the VOC's net value seems to have come to just over 0.1% of a world GDP which may be reckoned in modern prices at $6-700bn around the time of the company's commercial peak, so that the VOC may have been worth about $6-8bn in modern terms, close to your higher estimate (whoever thought Walmart could be so useful to the 18th-century economy?).

These conversions are all of course ultimately nonsensical: the economies of the 17th-18th and 21st centuries are just too different for any such result to count for anything much. But we know it wasn't the preposterous alleged $8 trillion!