What's an example of a really bad private equity deal?

The largest leveraged buyout in history was so bad, even Warren Buffett got nicked

This is a story about how private equity hubris, industry deregulation and “non-traditional” innovation all came together to eventually bring down what was once one of the largest power companies in the world.

It starts off as several disparate, seemingly unrelated stories but I promise that it eventually comes together.

If you follow along all the way to the end, you will see what happened when an eclectic group of wildcatters, power industry titans and (mostly) men from the world of high finance got together in the flatlands of North Texas and tried to do something that had never been done before.

(1) The Wildcatters

If you drive about fifty minutes northwest of downtown Dallas, you will see a landscape dotted with rectangular patches of yellow-gray gravel. These rectangular gravel fields are called “well pads” and are locations where a hole has been drilled into the ground to extract natural gas.

With modern technology, this is even easier to view from above — click on this Google Maps link and you will notice a bunch of various-sized rectangles distributed quite evenly across the map.

Now zoom all the way in; this is what you get to:

Partially fenced-off gravel fields are not uncommon sites in the oil-rich basins of Texas but people are generally more familiar with the traditional oil pumpjack:

Instead, these natural gas well pads look more like this from the ground:

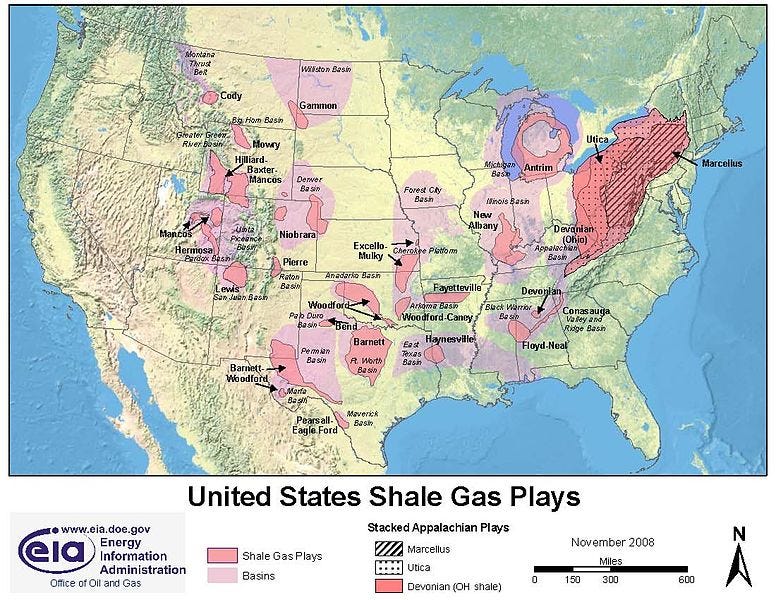

It was here in a geological formation called the Barnett Shale that Texas oilman George P. Mitchell found himself searching for natural gas on acreage that had long been drained of its “easy” oil — the type trapped in big underground pools where all you really had to do to recover it was stick a pipe in the ground. Geologists knew that there were still massive amounts of gas trapped in these large shale rock deposits but after a century of trying, still had no idea how to extract it economically and at scale.

The son of an illiterate Greek immigrant named Savvas Paraskevopoulus, Mitchell stubbornly clung to the idea that he could tap into this rock and extract this gas. Throughout the 80s and 90s, he experimented over and over again with different drilling techniques.

For example, instead of drilling straight down, he started drilling horizontally once he hit the shale formation. All sorts of weird materials were poured into the hole to see how they might coax the natural gas out of the shale. Tremendous pressure was exerted and explosives used to see if they could open up cracks in these formations to allow the gas to escape. All of these techniques had been used before in traditional oil and gas drilling but it was the creativity and sheer tenacity that Mitchell and his employees used to eventually figure it all out.

One day in 1998 a Mitchell Energy petroleum engineer named Nick Steinsberger headed over to a well called the S.H. Griffin #4. He had been experimenting with a novel idea. Instead of using a gel-like chemical substance to keep tiny fissures in the shale formation open to allow gas to escape, he had been experimenting with water. The gel-like substance had proven to be effective at allowing gas to escape for a short period of time before tailing off rapidly. The theory was that while the gel (and sand) would help keep the various rock fissures open long enough for the gas to escape, after a while the formation would just get gummed up and any remaining gas would be stuck. So you would have to drill and crack the formation again to extract more, and drilling cost time and money.

At S.H. Griffin #4, Steinsberger noticed that the well had continued to produce gas well beyond the typical gel frac. Total gas output had exceeded previously fractured formations by several times. On top of this, a water-based frac was significantly less expensive than a gel frac. The hydraulic fracturing code had been cracked and it would change the industry forever [Note i].

As an aside, the zoomed-into well in the Google Maps link above is the S.H. Griffin #4 wellpad.

(2) The Power Utility

On November 4, 1879, Thomas Alva Edison filed a patent for “an electric lamp using a carbon filament or strip coiled and connected to platina contact wires”. Three years later, electricity arrived in North Texas when the Dallas Electric Lighting Company began providing service to the city of Dallas, at that point a city of a little over 10,000. In the following years, cities throughout Texas lit up one-by-one.

For more than a century, these utilities powered their respective cities and by the 1980s, they had merged together into the consolidated Texas Utilities Electric Company. At this point, the company was the largest provider of electricity in the state of Texas, the second-largest state economy in the United States.

Its power generation relied heavily on coal which at the time was by far the least expensive form of electricity generation. It was a vertically integrated utility, meaning that it also provided transmission and distribution of electricity as well as marketing for end customers.

Traditional power utilities are very stable, boring businesses. They are natural monopolies (no need for redundant, multiple power lines into a home or business) and are regulated businesses that are allowed by the regulator (PUHCA) to generate a specific, typically modest rate of return.

Industry deregulation in the 1990s started to add a bit of excitement into these heretofore boring businesses. Suddenly, they were allowed to diversify outside of their geographic zones and also into other sectors. Power companies diversified into new areas (e.g. oil and gas pipelines), acquired other utilities, built trading operations and invested in greenfield speculative projects. In the late 1990s, Texas Utilities bought a large number of international assets, re-branded itself as TXU and by 2000 was the fifth-largest power company in the world.

With the collapse of the most aggressive of the Texan energy companies, Enron Corporation, industry deregulation ground to a halt in the early 2000s. Eventually, TXU divested itself of its international properties and pretty much went back to being a “boring” power utility. But one deregulation measure that stayed in place was the fact that retail marketing was opened up to competition. This comes into play later in this story.

(3) Base loads, Mid-Merits, Peakers, and the Spread

It was the summer of 2001 and I was starting my first real job as an investment banking analyst.

For a few months before I was to ship out to Hong Kong for my permanent posting, I did my analyst training in New York and was attached to the power industry group. It was here that I learned a few interesting things about the way the power industry worked. As it relates to this story, the most relevant piece was about how electricity was priced in the United States.

There are different ways to generate electricity — each with their own unique characteristics:

Massive nuclear plants that produce electricity at a very low marginal cost and take a long time to power up and shut down. The construction cost of these plants (measured on a $/megawatt basis) is very high and the shutdown and rehabilitation costs even higher.

Large coal-fired plants that also produce electricity very inexpensively — because coal is cheap and plentiful — and also take a long time to power up (although not nearly as long as a nuclear plant). Capital costs are high albeit not nearly as high as nuclear.

Hydroelectric plants that are expensive to build up-front but then cost very little to operate. They are great if you have them but unfortunately for the relatively flat Texas there aren’t a lot of places where the water flows fast enough to build them.

Then there are natural gas-fired power plants which are less expensive to build and easy to turn on and off. But they depend heavily on cost and access (via pipes) to a steady supply of natural gas.

There is also, of course, wind and solar, but for the purposes of this story we can ignore them as they made up a minuscule percentage of overall generation until only recently.

I also learned that electricity demand is not flat. It varies depending on time of day and also throughout the year (e.g. air conditioning drives electricity usage to be highest in warm states like Texas). Here is what the electricity usage curve might look like on a typical hot summer day in Texas:

Since electricity cannot be stored at this level of scale without tons of battery storage (which is still expensive) — one of the main jobs of the power utility is to manage power generation throughout the day and throughout the year. The way that power companies do this is by splitting up their generation assets into different types:

Base load — these run all of the time and typically feature the lowest variable cost (e.g. coal, nuclear and hydro). Dependable, consistent and low-cost electricity that is run at maximum output.

Mid-merit or “load following” — these are ramped up during the day and typically feature more expensive fuels. Natural gas is particularly suited for this role but coal (certain types that are easier to ramp up), hydro (you can stop and open the floodgates pretty quickly) and diesel can also be used.

Peakers or “peaking power plant” — generally run when there is high demand, like at 3pm on a hot summer weekday. Again, natural gas is great at this because it can ramp up very quickly (gas turbines are like big versions of the combustion engines in a gasoline-powered car; think about how little time it takes to start your car).

You end up with an operational plan that looks something like this:

The price of electricity is typically based on the total operating cost of the system. Besides the up-front capital cost, the main cost items are fuel costs, operating and maintenance, and the distribution network. Pricing the distribution aspect of electricity is a relatively straightforward return on capital (required to build out and maintain the transmission and distribution network) calculation. Pricing the generation aspect is a little more complicated because you are dealing with different types of fuel at different times of the day.

In general, power companies are allowed to price electricity generation at the marginal cost of electricity. This means that during low demand times, when most of the electricity being generated is base load, the marginal cost is quite low. At times of high peak demand, when your most expensive mid-merits and peakers are all firing, the marginal cost of electricity can be quite high.

One of most important implications of this is that for baseload generation, you are earning a lot more profit during peak demand periods than you are during low demand periods. Just how much more depends on the spread between the fuel cost of your peakers and the fuel cost of your base loads.

For the state of Texas, the spread was the difference between the price of coal (used for base load) and natural gas (used for peakers). And this is where the paths of the staid power guys and well-heeled buyout masters began to converge.

(4) The Masters of the Universe

Many people point to the year 2007 as the cyclical peak of the buyout industry. The post-9/11 economic downturn and subsequent Fed response (lower interest rates) had combined to create many attractive opportunities to buy attractive businesses with low-cost leverage. The economy was now firing on all cylinders, driven in part by the housing boom, and things had never looked rosier for the buyout kings, also referred by some at the time as “Masters of the Universe” [Note ii].

At this point in time, I was also an aspiring Master myself, working for the technology investing group of a mid-sized private equity firm. It was from this perch that I had watched the industry expand rapidly in the post-9/11 years.

Deal sizes expanded, exit IRRs/multiples impressed and we saw the first mega-funds (i.e. over $10 billion) emerge. For a time it seemed like every month there was another record-setting buyout deal. 2007 was one of the largest payout years for carried interest checks. Blackstone went public in a $4 billion IPO. The large buyout firms expanded from funds measured in the billions to funds measured in the tens of billions in short order.

But deploying tens of billions of dollars of equity is not easy when you are looking for “traditional” private equity deals. To soak up that much capital — and get to the next fund — you had to start looking at larger companies which meant trawling in the public markets. You also had to start thinking a bit more creatively and expand your comfort zone.

It was around this time that private equity firms turned their eyes to the power industry. Historically, they had stayed away from power companies because the industry was highly regulated and the capital requirements were high. Also, the traditional utilities already ranked amongst the most highly leveraged industry sectors due to the stable cashflow these types of businesses generated.

But now, armed with enormous funds, the private equity firms were ready to dip their toes in the water. It helped that less than two years earlier, some of these funds had made more than five times return on their investment in a merchant power generation company in Texas in the span of 18 months in what was one of the most lucrative private equity deals that year. Some of the firms that participated in that deal decided to see if lightning could strike once again.

(5) The Largest Buyout in History

On February 26, 2007, TXU Corp. agreed to be acquired by a consortium of private equity investors led by legendary buyout firms Kohlberg Kravis Roberts and Texas Pacific Group. At a $45 billion valuation it was the largest buyout in history. The company was renamed Energy Future Holdings.

The transaction was funded with over $35 billion of debt and required significant regulatory concessions. After the transaction was completed, the business was separated into three distinct businesses: a regulated transmission business (Oncor), a retail electric provider (TXU Energy) and a power generator (Luminant).

As I alluded to earlier, the regulated transmission business is a cost of capital business. This means that the amount of money you are allowed to make by the regulators is relatively fixed. It is a very stable business where it is hard to make or lose that much money.

However, the other two businesses were more volatile, especially after deregulation of retail pricing from earlier in the decade:

You generate revenue by selling electricity at prices that are set according to a formula based on the marginal price of electricity. Remember that daily electricity demand curve from above? During peak hours (9am to around 7pm), peakers set the marginal price of electricity — and most of these peakers used natural gas.

On the cost side, the main variable expense was fuel. For Energy Holdings, this was coal.

Putting two and two together, the profitability of the company — and ultimate investor returns — depended largely on the spread between natural gas and coal prices.

Coal is inexpensive and prices are fairly stable — power companies try to lock in very long-term supply agreements. Natural gas prices were more volatile, although they can be hedged.

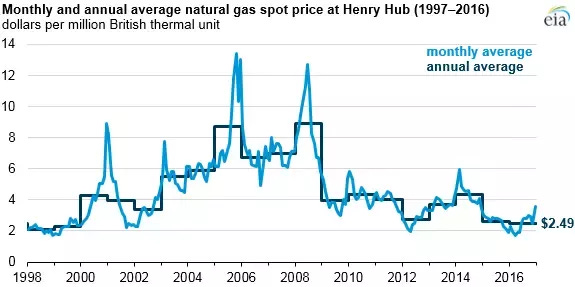

At the time of the deal, natural gas prices were around $7 to $8 per million BTUs. This was up from $2 to $3 a decade earlier as demand for natural gas, a cleaner alternative to coal, had increased significantly.

By mid-2008, prices had spiked to $13 per mmbtu. Energy Future Holdings and its investors were excited about the prospect of a massive payday on the horizon.

(6) Boom and Bust

As you probably guessed from the question, that turned out to be a very short-lived peak. Natural gas prices plunged shortly thereafter.

What happened?

First, the economy collapsed — triggered by the now infamous real estate bubble. Plummeting economic activity led to reduced electricity demand and demand for natural gas. By 2009, natural gas had plummeted back to $3 per mmbtu.

But prolonged economic downturn on its own — even one as harsh as the Global Financial Crisis — should not have been enough to cause the downfall of Energy Future Holdings. Private equity folks are keenly aware of the risk of economic recessions and the Energy Future investors had planned accordingly.

If there is one thing that private equity folks know well, it is financial engineering. Sensitive to the risk of a decline in natural gas prices, the investors used financial instruments to hedge the natural gas prices such that they would still be able to maintain the spread and remain profitable for a period of time. The idea was that the economy would eventually recover and natural gas prices along with it.

The problem is that even though the economy eventually did recover, natural gas prices did not:

Natural gas prices cannot be hedged forever. Eventually its derivatives expired and Energy Future began bearing the full financial brunt of depressed natural gas prices. Operating margins plummeted. Interest expenses had risen more than fivefold as private equity investors had loaded the company with debt. The company began to generate massive losses. Equityholders were wiped out. Soon, bondholders were at risk as well. Even secured lenders did not escape unscathed.

Warren Buffett had invested $2 billion in Energy Future bonds as part of the buyout. In his 2011 Letter, he admitted that this was a “big mistake” and a major “unforced error”. Those bonds were eventually sold at an $873 million loss.

(7) Conclusion

So what happened here? Why did natural gas prices never recover?

This is a good time to check back in on those oil wildcatters from the beginning of the story.

After the discovery of how to use water to frac a shale formation at S.H. Griffin #4, it became economical to recover natural gas from shale formations. In the ensuing years, the technique was refined and improved. Eventually the wildcatters even figured out how to get oil out of these shale formations.

And as it turns out, these shale formations are massive and widely distributed throughout the country. God truly did shed His grace on America, for beneath the “amber waves of grain”, “fruited plains” and majestic “purple mountains” lay some of the largest reserves of unconventional oil and gas on the planet.

Unlike conventional oil and gas exploration, the risk of drilling a dry hole was much lower. This made it easy for capital to enter the space and the result was steadily increasing supply of economical gas (not to mention shale oil as well). All of this accessible supply meant that it was highly likely that low gas prices were here to stay.

In other words, this was a permanent and not a cyclical trend that could be hedged out. And it was ultimately the result of good ol’ American ingenuity and innovation.

Yes, “innovation”. Some may balk at the use of this word when applied to the oil and gas industry and George Mitchell may not look like your typical entrepreneur. But in my view, Mitchell should be celebrated alongside Bill Gates and Steve Jobs in the pantheon of great American entrepreneurs. Figuring out how to extract oil and natural gas out of shale rock was one of the most significant American innovations of the last two decades:

Lower, less volatile energy prices for all.

Natural gas is a lot cleaner than other fossil fuels, and replacing dirtier sources has a net positive environmental benefit.

Even more significantly, it has reduced our economic dependence on others. We are even starting to export it.

It is easier to avoid geopolitically volatile regions like the Middle East and hopefully leads to fewer pointless conflicts.

Energy independence was a big topic of discussion around election time 15–20 years ago. Now, nobody really brings it up anymore because we are nearly there and it is no longer such a big source of anxiety.

The private equity investors and bondholders had not properly factored in the potential for innovation to completely change the rules of the game. One thing I noticed working in the industry was that traditional private equity guys tended to be value-oriented and while they are great at thinking about and pricing in all sorts of risk, innovation and disruption are two things that they often miss. As Mr. Buffett himself wrote in that 2011 letter: “I totally miscalculated the gain/loss probabilities [of natural gas prices] when I purchased the bonds.”

There are other lessons here (e.g. the heightened risks of too much debt, mistaking secular trends for cyclical ones, second-order effects, sticking within your “circle of competence” etc.) but I think a key, under-appreciated lesson is that innovation can be hard to predict. Lightning can strike anywhere, with little warning. But just because it is hard to predict doesn’t mean it can be ignored. As an investor, it is very important to recognize true innovation/disruption when it does happen and react/adjust accordingly.

In particular, American ingenuity has proven time and time again its ability to surprise and throughout history it has been a far more profitable wager to bet on it rather than against it.

Notes

[i] The George Mitchell and Mitchell Energy story is detailed in the excellent book about the pioneers of fracking The Boom by Russell Gold. The Nick Steinsberger story is also mentioned in the book as well as a 2013 feature story in The Atlantic.

[ii] Original reference to famous phrase used in Tom Wolfe’s novel The Bonfire of the Vanities.

This was originally published on Quora in October 2018.