What does the bike-sharing mania say about the Chinese economy?

The convergence of multiple China themes

There are so many themes one can expound on related to the recent dockless bike-sharing phenomenon in China. We can talk about the rise of consumption and the service sector, unique aspects of its sharing economy, the ruthlessly competitive nature of “Capitalism with Chinese characteristics”, whether or not China is in a bubble, the upsides and downsides of a rapidly evolving modern Chinese society etc. But for this answer I wanted to zero in on the following themes:

Mobile payments as the key enabling “Platform Technology”

“Game of Thrones” starring Alibaba and Tencent

The importance of scale

“To the Victor belongeth the (massive) Spoils of War”

Before I delve into these, I wanted to first take a closer look at dockless bike-sharing model itself and explain why I think it will eventually emerge as the dominant form of bike sharing in China as well as in cities around the world.

Some Background on Dockless Bike-Sharing — and how Mangled Bikes in the early 21st might be a bit like Tangled Wires in the early 20th

As you can probably figure out from the name, the key difference between dockless bike-sharing and traditional bike-sharing is eliminating the docking station. Instead, an electronic lock is placed on the wheel of a simple one-speed bike and users use their mobile phone to unlock the bike. This lock can communicate with the network to update the bike’s status in real-time. Here is what it looks like:

To gain access to the bike, you scan a QR code on the bike and, if valid, the app returns a 4-digit PIN code that you can use to open the lock. When you are finished, you merely close the lock and the bike tells the system that the trip is completed and it is now available again.

There are several significant differences between the dockless approach vs. traditional bike-sharing:

First, a traditional docking station based system means that riders need to go to specific areas in the city to pick up and drop off their bikes. Often the docking stations are full so you have to go find another docking station to complete the transaction. The traditional bike sharing companies developed apps to tell you where there are open docking stations but the overall experience is still much less convenient than being able to drop off the bike pretty much anywhere and avoiding that anxiety. From the rider’s perspective, dockless bike-sharing is far more convenient than traditional bike-sharing — which leads to far more frequent use.

Second, you save a massive amount of upfront capex by eliminating the docking stations. Installation of the docking stations is the most expensive part of the system — you need to apply for permits from the city, build customized docking stations that fit your bikes (not to mention custom fixtures on the bikes themselves), connect it to the electrical and communications grid etc. With dockless bike-sharing all you need to create a designated bike zone is a few bucks for some white paint and kindergarten-level art skills to paint a rectangle on the ground. Instead of spending say a hundred thousand dollars on a 10-bay docking station you could use the capital to put 500 bikes on the street at $200 a pop. For the same cost it took to build New York’s 12,000 bicycle Citibike network (est. $200 million [1]), you could put more than half a million bicycles on city streets throughout China. Being able to put 50x the number of bikes on the street for the same price means you can lose half of them and still come out way ahead. See Note 2 below for additional details about how this massive difference in investment cost shows up in end-user pricing.

Third, the docking stations are expensive to maintain as they are located outdoors and subject to rain, wind, snow and other climate extremes. They break down quite easily and require significant ongoing maintenance — money that can instead be used to maintain or replace older bikes in a dockless system.

Fourth, docking stations take up a ton of valuable urban sidewalk space — you can fit at least double the number of dockless bikes in the same space taken up by those bulky docking stations.

Fifth, under a docking station system, you really only allow room for one real player in the market. There is much less room for competition meaning slow roll-outs, higher costs and greater risk of rent-seeking type behaviour once installed.

It is no surprise that usage exploded virtually overnight. Dozens of bike-sharing companies emerged, some raising hundreds of millions or even billions of dollars to flood Chinese city streets with bicycles. Consumers quickly adapted their daily commutes and activities to this new transit option.

Rapid change is often accompanied by negative ramifications as well, and it has been no different with dockless bike-sharing. The flood of bicycles clogged sidewalks and pedestrian routes. Intense competition invited ruthless and unethical behaviour. Many bike-sharing companies could not keep up with the competition and started going out of business, most recently with Bluegogo.

While some are pointing to Bluegogo's demise and the iconic picture of the bicycle graveyard (above) as an indicator that the endeavor was a big waste of time and money, my view is that dockless bike-sharing is here to stay.

Indeed, when I thought of the current state of the industry, it reminded me of what I imagined it was like shortly after the invention of the telephone, when dozens of phone companies strung their own wires up in cities around the world, leading to scenes like this in New York City:

Eventually, the industry consolidated and regulators stepped in with rules to govern the industry, and ultimately ushered in the era of “instant remote communication” changing people’s lives forever. People adapted their behaviour to this new invention, developing rules and etiquette for how to talk to each other over the phone and over time, it became ubiquitous and just another piece of the fabric of modern society. While I do not mean to imply that dockless bike-sharing is going to have the same impact on the world as the telephone, I do think the industry will follow a similar path — a messy fast-growth “land grab” phase followed by consolidation and eventual equilibrium.

Consolidation — which has already happened to a large extent — will improve the underlying economics of the business model. Reducing the number of players down to two to three for any given market will also reduce the amount of ruthless competitive behaviour that we have seen thus far. The eventual winners will have to learn how to coordinate better with city transit officials so that bikes can be better integrated with the public transportation system. Riders will have to learn new rules of etiquette governing where it is okay and where it is not okay to ride and park the bikes. It might take some time but over time I am pretty sure dockless bike-sharing will win out and permanently change urban transit not only in China but also eventually in cities around the world.

Mobile payments as the key enabling “platform technology”

Why did dockless bike-sharing emerge in China and not anywhere else?

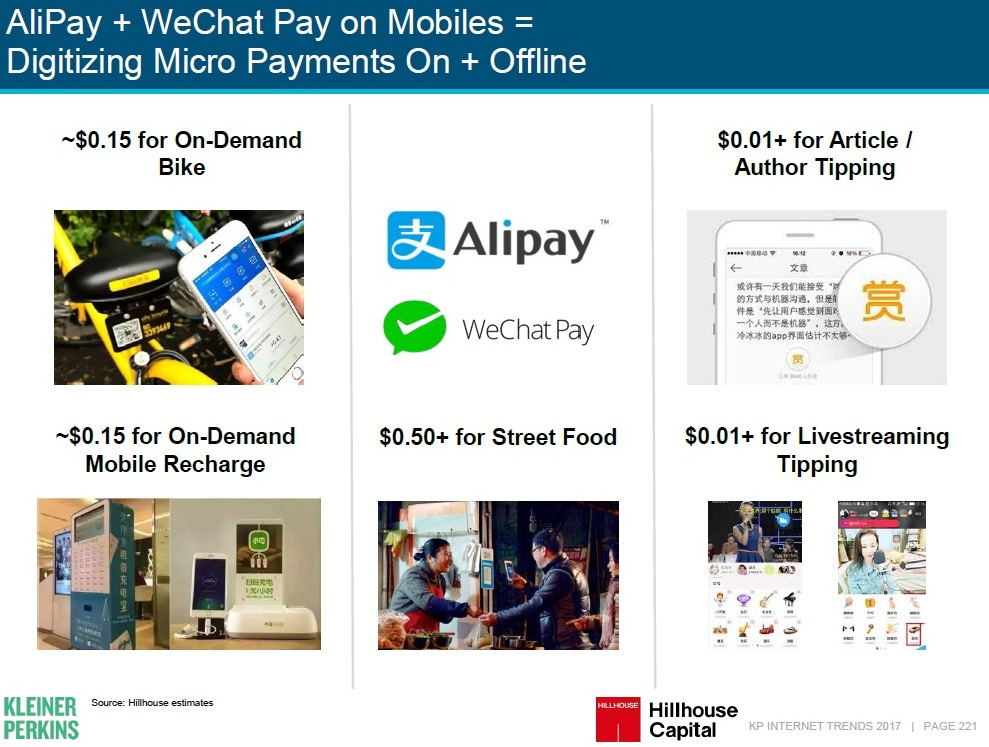

The main reason is that the success the dockless model was highly dependent on the ability to make mobile QR-code based micro-payments. In other words, dockless bike-sharing emerged because of the emergence and rapid adoption of Alipay and Wechat Payments from 2013 to 2016.

Traditional bike-sharing services required docking stations because there was no economical way to lock and unlock bikes on the bike itself. Without a QR-based identification solution, it was prohibitively expensive to build electronic ID units into the bikes themselves — so the brains had to built into the docking unit itself.

I remember signing up for Citibike in New York City when it first rolled out and they would issue a RFID-based ID keychain that could be used at docking stations to access bicycles. You had to pay an annual subscription cost of around $100 for unlimited use of bicycles [2]. Out-of-towners or pay-as-you-go riders who wanted to use Citibikes had to register at a kiosk that was located at each docking station. There you would input your credit card information and then be given an access code to one of the bikes. UBike in Taipei — which I also used — had a similar system albeit a little more efficient because it integrated with Taipei’s RFID-based metro card.

QR-code based micropayments removed all of this hassle and up-front commitment. If you had Alipay or Wechat Payments, all you had to do was link it to the bike-sharing app (which could also be located within Alipay or Wechat itself) and immediately be on your way to unlocking a bike. Meanwhile, credit cards have a hard time processing micro-payments because its fee model is comprised of a fixed fee (around 30 cents) plus a percentage of transaction value whereas merchants have no problem processing Alipay and Wechat Payments — you can send 0.1 RMB (i.e. a little over a penny) to someone if you wanted to (which as an aside, has become a new tipping-based business model for new activities such as livestreaming).

When I was in middle school, I remember playing a game on my PC called Sid Meier’s Civilization where you would guide and build a tribe into a great modern civilization and beyond. In the game, to get to the next level of advancement, you had to first acquire all of the pre-requisite technologies and inventions. For example, to get “Literacy” you needed “Writing” and a “Code of Laws”. From “Literacy” you could later enable “Invention” and from there you could get to “Gunpowder” and on and on.

In a similar way, the invention of dockless bike-sharing was made possible only after a modern mobile payments infrastructure had been put in place. Just like mobile payments itself as enabled by the proliferation of another platform technology, the smartphone.

Mobile payments is a true platform technology just like the telephone, electricity or mobile broadband and China is so far ahead of everyone else in the world on this that it isn't even funny: aggregate transaction value processed on Alipay and Wechat Payments ($8 trillion per annum) has surpassed that of the entire global credit card industry and will probably double again in the next two years.

Dockless bike-sharing will only be one of dozens of innovative new business models that are built on the back of mobile payments platform technology.

“Game of Thrones” starring Alibaba and Tencent

From their commanding heights at the centers of e-commerce and social media, respectively, Alibaba and Tencent are playing the role of kingmakers in China’s modern-day economy.

As discussed in the previous section Alipay and Wechat Payments essentially made dockless bike-sharing possible at scale. But they bring more than just the platform technology. Through their core e-commerce and social media businesses, respectively, Alibaba and Tencent have massive user bases and access to massive amounts of proprietary data. If you want to scale rapidly, your best bet for rapid customer acquisition is to rely on one or both Alibaba/Ant Financial and Tencent. It should be little surprise then that the two leading bike-sharing companies in China (Ofo/Alibaba/Ant and Mobike/Tencent) count the two Kingmakers among their investors.

This has happened time and time again across multiple Internet/O2O business models from car sharing (Didi, Kuaidi) to food delivery (Meituan, Koubei/Eleme) to grocery (Sunart, JD Fresh) and abroad in Southeast Asia. In almost every emerging industry, Alibaba and Tencent have picked their horses and are squaring off in a battle for ultimate supremacy (or if things get too competitive, just merge e.g. Didi/Kuaidi). In the battle between these two heavyweights, it is very common for non-affiliated independents to get taken out by collateral damage — the most recent example being Bluegogo.

The Importance of Scale

China is big. To win in many industries, you need to “go big or go home”. Let's take a look at the economic and strategic benefits of scale in the dockless bike-sharing business model.

First, scale allows you to negotiate with your suppliers. You will have better pricing on your bikes if you can put in a hard order for 1 million bikes instead of one for a “mere” 50,000 bikes. Scale will allow you or your manufacturer to procure components less expensively, amortize overhead and run the factory more efficiently. Over time you may be able to work closely with your manufacturer to drive down costs. In the cutthroat world of bike-sharing, every RMB counts.

Second, higher density and coverage at the street level means your customers will be able to more easily find bikes to ride. If you have half the number of bikes as a competitor, then riders are much more likely to eventually make that app the default choice when they need a bike. It’s kind of like how even if Bing’s search results are just as good as Google’s everyone still just goes to Google out of habit.

Third, once you achieve scale at the local level, you will start to build up significant amounts of customer ride data. This data can be used to optimize the network — as an example, moving bikes en masse to certain high-traffic locations in anticipation of demand surges. It can also be used to more efficiently maintain the network — e.g. optimizing routes for maintenance crews. And then, over the long run, as you collect some very unique data on your customers, you can start to undertake some very interesting marketing activities.

These three points are very common success factors that are related to scale that you can see across many emerging business models in China. That is why scale is so important, and why companies compete so hard to achieve scale. It is why customer prices may seem absurdly low (or come with massive marketing discounts) during the “land grab” phase and why companies are willing to lose money for an extended period of time. Because if they can outlast their competitors ...

“To the Victor belongeth the (massive) Spoils of War”

The rewards for winning in China are massive. One in three “unicorns” is now in China and that proportion will probably only rise in the coming years.

Investing a few billion dollars in bike-sharing and flooding the street with millions of bikes might seem crazy. But think about how valuable the company that emerges as a winner alongside one or two other winners as the industry settles into a stable oligopoly.

In the ride-hailing business, Didi, Kuadi and Uber raised and spent upwards of $15 billion fighting a multi-year battle for supremacy in China. Didi and Kuadi merged and then Uber gave up in exchange for a minority stake in the combined entity. Today Didi Chuxing is one of the world's most valuable unicorns and given Uber's recent troubles it has probably surpassed Uber as well (ironically, one of the most valuable parts of Uber’s valuation may ultimately be the significant stake it holds in Didi Chuxing). Losing a couple billion a year for a few years makes sense if it ultimately gets you a seat at the winners’ table and a $50 billion or $100 billion valuation.

The same things can be said for the bike-sharing industry. The two largest players with the most funding are using their scale advantage to bleed out their competitors until there are only two or three players standing. At that point, pricing will go up and there won’t be an over-supply of bikes on the street. And the winners step forward and claim their place amongst the world’s most valuable unicorns at that point.

Notes

[1] Total investment in Citibike has been around $200 million and currently the total system capacity is around 12,000 bicycles. This comes out to around $17,000 per bicycle / docking station. It is less expensive to build docking stations in China but $10,000 sounds like the right order of magnitude. Source: Wikipedia

[2] Unlimited use as long as each trip was under 45 minutes. Today the cost is $163 per year. A day pass costs $12. If you rented a dockless shared bike in China for an entire 24-hour period (and did not log in and out), it would cost 48 RMB ($7.20). In reality, you are probably going to ride a bike for at most two hours which would cost you 4 RMB (60 cents). This huge price difference reflects the vast difference in economics between the two models.

This was originally published on Quora in November 2017.